Chapter 5 Process Data in R

R specializes in data processing, encompassing a wide range of operations such as downloading, importing, cleaning, merging, transforming, summarizing, analyzing, and visualizing data. Previous chapters have introduced the core functions for performing these tasks (refer to Chapter 3 and 4). This chapter takes a practical approach by applying these concepts to real financial datasets in three illustrative examples. The key tools introduced in each example are summarized in Table 5.1.

| Data | Import Format | Tasks | |

|---|---|---|---|

|

|

Bitcoin prices |

DSV file

\(\downarrow\) data.frame

|

|

|

|

Stock and oil prices |

Web API data

\(\downarrow\) xts

|

|

|

|

House prices |

Excel workbook

\(\downarrow\) tibble

|

|

As shown in Table 5.1, each example leverages different file types, data structures, and tools. Example 1 manipulates data frames using base R, as introduced in Chapter @ref(data.frame). Example 2 employs xts objects, detailed in Chapter 4.8. Example 3 utilizes Tidyverse functions on tibbles, as discussed in Chapter 4.6.

New in this chapter is the focus on data import methods. Example 1 deals with DSV files, including CSV and TSV. Example 2 retrieves data via Web API. Example 3 deals with Excel workbooks. For importing data formats not covered here, search “import data in R” along with the format name in Google. You’ll likely find a dedicated package for the task. For instance, the DBI and RSQLite packages facilitate SQL database imports, while haven enables importing SPSS, SAS, and Stata files.

Additionally, this chapter expands on visualization methods beyond those covered in Chapter 3.4. For instance, Example 2 introduces plot.zoo() for graphing xts objects, and Example 3 incorporates advanced plotting via the ggplot2 package.

5.1 Process Bitcoin Price Data

This section demonstrates how to process Bitcoin prices from the Bitstamp exchange, obtained from CryptoDataDownload (Bitstamp 2024). Once the data is downloaded as a CSV file, it is imported into R. The date column undergoes conversion to a POSIXct data type. Subsequently, the data is visualized and exported in both RDS and CSV formats.

5.1.1 Download DSV File

The procedure to obtain this dataset is detailed in Chapter 3.7.3. Briefly:

- Visit www.cryptodatadownload.com.

- Navigate to “Historical Data” > “US & UK Exchanges”.

- Click on “Bitstamp”, then find the “Bitstamp minute data broken down by year” section.

- Choose “BTC/USD 2023 minute” and click “Download CSV”.

After downloading, ensure you place the file in your R working directory, specifically inside a folder named “files”, and rename the file to BTCUSD_minute.csv. For information on how to identify and set your working directory, refer to Chapters 3.7.1 and 3.7.2.

5.1.2 Import DSV File

In R, datasets are primarily stored and manipulated using two-dimensional structures such as matrices and data frames, complemented by extensions such as tibbles, data tables, and xts objects. Various functions exist for importing external datasets into R. The choice of function depends both on the external dataset’s format, whether CSV, Excel, or XML, and the intended data structure in R, whether a data frame, matrix, tibble, or xts object.

DSV (delimiter-separated values) is a common file format used to store tabular data. As the name suggests, the values in each row of a DSV file are separated by a delimiter. This delimiter is a sequence of one or more characters used to specify the boundary between separate, independent regions in a data table. Depending on the character used as a delimiter, different notations emerge, such as CSV (comma-separated values) and TSV (tab-separated values). Sometimes semicolons, spaces, or other characters are used as delimiters in similar formats.

Here’s an example of how data is stored in a CSV file:

Gender, Age, Score, Rank

Male, 25, 100, 3

Female, 22, 90, 4And for a TSV file, the data would look like this:

Gender Age Score Rank

Male 25 100 3

Female 22 90 4Note the use of tabs in the TSV example to separate the data fields, in contrast to the commas used in the CSV example.

To read DSV files into R and convert them to data frames, the read.table() function comes in handy. The function has several arguments that allow customization based on the structure and specifics of your DSV file. Before importing, it’s advisable to preview your DSV file in a spreadsheet program like Microsoft Excel to understand its layout and structure.

Here’s an illustration of how to employ the function using the downloaded BTCUSD_minute.csv file:

# Load DSV file containing Bitcoin prices

btcusd <- read.table(

file = "files/BTCUSD_minute.csv",

sep = ",", # Delimiter is a comma (CSV)

header = TRUE, # The file has a header row with column names

dec = ".", # Decimal point character is a period

na.strings = "NA", # Character string representing NA values

skip = 1, # Skips the introductory row (website's name)

nrows = 5000 # Limits reading to the initial 5000 rows

)

# Display the first 4 rows of columns 1 to 7 for an overview

btcusd[1:3, 1:7]## unix date symbol open high low close

## 1 1697413380 2023-10-15 23:43:00 BTC/USD 27114 27119 27107 27119

## 2 1697413320 2023-10-15 23:42:00 BTC/USD 27114 27120 27114 27120

## 3 1697413260 2023-10-15 23:41:00 BTC/USD 27115 27119 27115 27119In this illustration:

file: Denotes the DSV file’s path and name.sep: The delimiter is a comma for this CSV file, i.e.sep = ",". For a TSV file, you would usesep = "\t". Ifsep = ",", theread.csv()function could be used similarly without the need for thesepargument.header: Indicates the presence of a header in the file. When TRUE, the row following the skipped rows (if any) is considered as the column names.dec: Specifies the character for decimal points. In the U.S., this is typically2.84withdec = ".", while in parts of Europe it’s2,84withdec = ",".na.strings: Sets the string that corresponds toNAvalues. Some datasets may use “N/A” or might leave the entry blank, leading to configurations likena.strings = "N/A"orna.strings = "", respectively.skip: States the initial lines to omit from the file.nrows: Caps the rows read from the file.

By tweaking these parameters, you can handle a wide range of DSV file structures and peculiarities.

It’s important to note that the read.table() function by default imports the DSV file as a data frame:

## [1] "data.frame"Once the data is imported, you can transform the data frame into various data structures:

- Convert to a tibble using the

as_tibble()function from thetibblepackage. - Transform into a data table via the

as.data.table()function from thedata.tablepackage. - Create an

xtsobject using thexts()function from thextspackage.

For more direct approaches:

- The

read_delim()function from thereadrpackage by Wickham, Hester, and Bryan (2024), part of the Tidyverse, directly imports DSV files as a tibble. - The

fread()function, found in thedata.tablepackage, imports DSV files as a data table. - To directly read DSV files as

zooobjects, one can use theread.zoo()function from thezoopackage. Subsequently, to transform thezooobject into anxtsobject, apply theas.xts()function from thextspackage.

While these functions share certain traits with read.table(), they also come with their own unique features. To fully understand their capabilities and differences, consider consulting their respective documentation using ?read_delim, ?fread, and ?read.zoo after loading the readr, data.table, and zoo packages.

5.1.3 Inspect Data

Once data is imported, a preliminary examination ensures its accuracy. This can be done by simply entering the data name btcusd into the console. However, since R prints the entire data frame, the columns will not be visible if the data contains more rows than the size of the screen. To accommodate this, you can use the head() function to print the column names and the first six observations, or the tail() function to print the column names and the last six observations, where the additional input n = 10 increases it to ten observations:

## unix date symbol open high low close

## 4991 1697099580 2023-10-12 08:33:00 BTC/USD 26799 26799 26799 26799

## 4992 1697099520 2023-10-12 08:32:00 BTC/USD 26805 26805 26805 26805

## 4993 1697099460 2023-10-12 08:31:00 BTC/USD 26796 26807 26796 26807

## 4994 1697099400 2023-10-12 08:30:00 BTC/USD 26789 26800 26789 26800

## 4995 1697099340 2023-10-12 08:29:00 BTC/USD 26794 26794 26794 26794

## 4996 1697099280 2023-10-12 08:28:00 BTC/USD 26798 26798 26796 26796

## 4997 1697099220 2023-10-12 08:27:00 BTC/USD 26786 26790 26784 26790

## 4998 1697099160 2023-10-12 08:26:00 BTC/USD 26790 26790 26790 26790

## 4999 1697099100 2023-10-12 08:25:00 BTC/USD 26790 26792 26787 26790

## 5000 1697099040 2023-10-12 08:24:00 BTC/USD 26778 26778 26777 26778In cases where numerous columns still prove problematic even with head() or tail(), RStudio provides a spreadsheet-like viewer for data frames via the View() function (exclusive to RStudio and not included in R):

For an exploration of the data’s structure and summary, execute str(btcusd) and summary(btcusd).

5.1.4 Clean Data

It’s important to check the data type of each column, as the import process may have misassigned data types. Utilize sapply() together with class() for this task:

# Examine the data structure of the dataset

class(btcusd)

# Identify the data type for every column

sapply(btcusd, class)## [1] "data.frame"

## unix date symbol open high low

## "integer" "character" "character" "integer" "integer" "integer"

## close Volume.BTC Volume.USD

## "integer" "numeric" "numeric"In this scenario, R has accurately discerned Bitcoin prices and trading volumes as numerical values. The columns open, high, low, and close denote the opening, peak, trough, and closing prices within a minute interval, respectively. Volume.BTC and Volume.USD quantify transaction volumes in bitcoins and USD.

However, the date column wasn’t identified as a specific date format, such as POSIXct. This requires manual conversion (refer to Chapter 3.3 for understanding date objects like POSIXct).

# Modify date strings to the POSIXct data type

btcusd$date <- as.POSIXct(btcusd$date)

# Recheck the data type of the date column

class(btcusd$date)## [1] "POSIXct" "POSIXt"Such type adjustments are common when importing data in R. When employing read.table() in R, the function inspects the first 1,000 rows to deduce each column’s type. If these rows aren’t indicative of the complete dataset, misinterpretations can arise. An example: if the initial 1,000 rows of a column seem numeric but later on contain a character, R might incorrectly perceive it as numeric, where the characters are converted to numeric NA values. Another scenario is R reading a column as character values when the first 1,000 rows of a column are absent, instead of numeric values. Also, R might read “N/A” as a character string instead of a missing value, causing the column to become character type instead of numeric. The last issue can be addressed by defining na.strings = "N/A" within read.table(), or by replacing “N/A” post-import with NA and then using as.numeric() to convert to numeric.

To improve data clarity, consider adding contextual attributes like the data source and the count of imported rows. These attributes can be easily appended using R’s attr() function. For a cleaner data structure, it’s also beneficial to eliminate the row.names attribute for our btcusd object, as it merely consists of sequential numbers. In R, setting an attribute to NULL effectively removes it.

# Attach source and row count as attributes to the btcusd object

attr(btcusd, "source") <- "www.cryptodatadownload.com/cdd"

attr(btcusd, "n_rows_imported") <- nrow(btcusd)

# Erase the row.names attribute

attr(btcusd, "row.names") <- NULL

# Examine attributes to confirm changes

attributes(btcusd)## $names

## [1] "unix" "date" "symbol" "open" "high"

## [6] "low" "close" "Volume.BTC" "Volume.USD"

##

## $class

## [1] "data.frame"

##

## $source

## [1] "www.cryptodatadownload.com/cdd"

##

## $n_rows_imported

## [1] 5000By doing so, anyone reviewing this data object can immediately understand its origin and size without having to consult external documentation. This additional layer of metadata can be especially beneficial when sharing data objects across different phases of a project or with other collaborators.

5.1.5 Visualize Data

A graph is a visual representation that displays data points on a coordinate system, typically showing the relationship between two or more variables. Each variable is assigned to an axis, and the data points are plotted accordingly. In R, the plot() function is one of the primary tools for creating graphs.

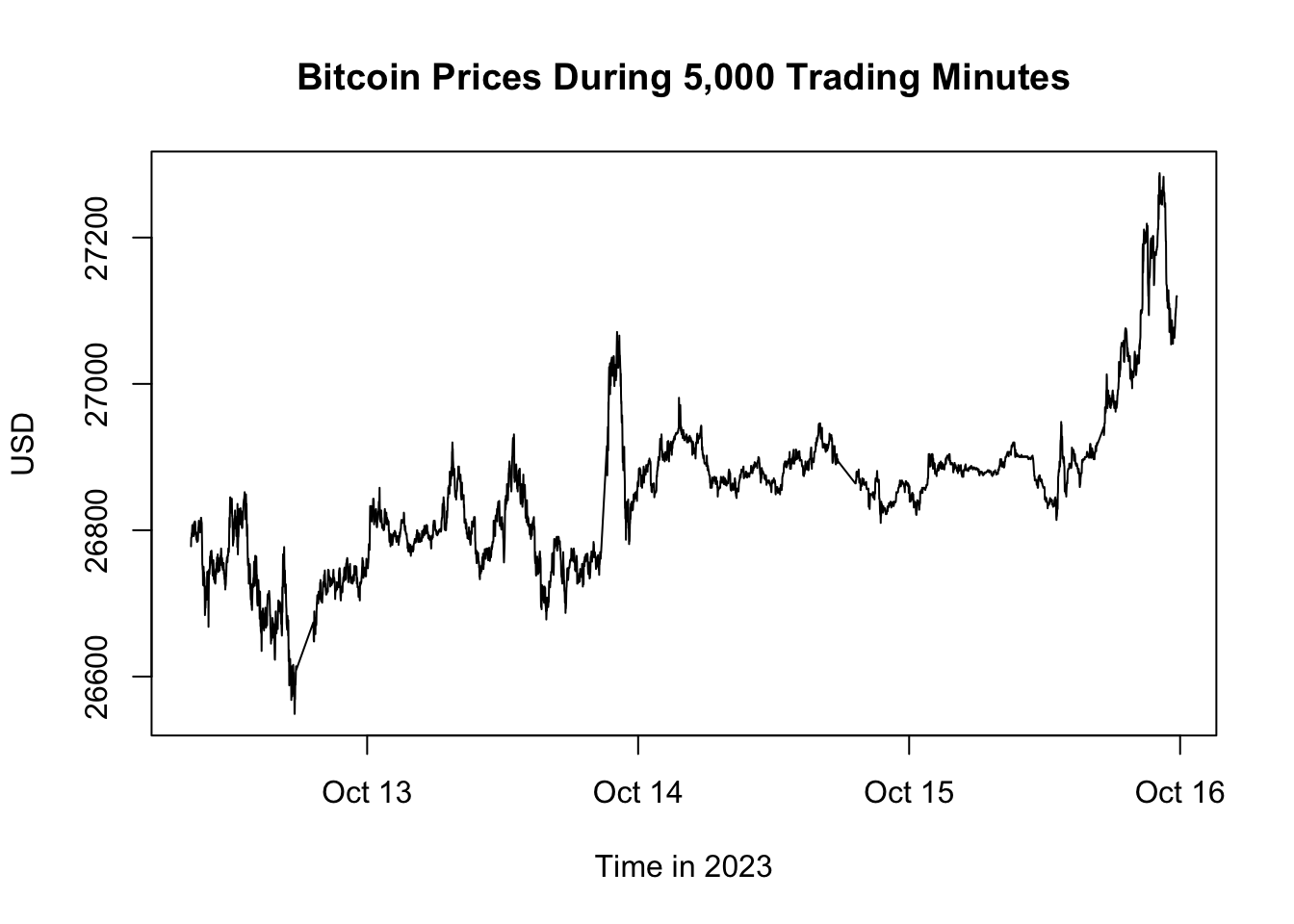

Consider the Bitcoin prices dataset, btcusd, from our previous section. We’ll map the date (btcusd$date) onto the x-axis and the closing price at each trading minute (btcusd$close) to the y-axis:

# Plot data

plot(x = btcusd$date,

y = btcusd$close,

type = "l",

main = "Bitcoin Prices During 5,000 Trading Minutes",

ylab = "USD",

xlab = paste("Time in", format(tail(btcusd$date, 1), "%Y")))

Figure 5.1: Bitcoin Prices During 5,000 Trading Minutes

Here’s a detailed breakdown of the plot() function arguments used in the example:

xandy: These are the primary arguments that specify the data for the x-axis and y-axis, respectively. In the given example,btcusd$daterepresents the time variable on the x-axis, whilebtcusd$closesignifies the Bitcoin closing prices on the y-axis.type: This argument determines how the data points should be represented. The value"l"indicates that the data points should be connected with lines, producing a line graph. Other common values include"p"for points (producing a scatter plot),"b"for both points and lines, and"h"for vertical lines (like high-density plots).main: This argument defines the main title of the graph. Here, “Bitcoin Prices During 5,000 Trading Minutes” serves as the title, succinctly conveying the subject of the visualization.xlabandylab: These arguments specify the labels for the x-axis and y-axis, respectively. Properly labeling axes is vital as it provides context and clarifies the variables being visualized. In our example, “Time in 2023” denotes the time intervals on the x-axis, and “USD” indicates that the y-axis represents Bitcoin prices in US dollars.

Figure 5.1 showcases the closing prices of Bitcoin over a span of 5,000 trading minutes. By visually inspecting the graph, one can gauge the volatility, identify any potential data inconsistencies, and generally understand the behavior of Bitcoin prices over the observed interval.

5.1.6 Export Data

This section shows how to export data in two commonly used formats: RDS and DSV.

RDS

R provides a unique storage format known as RDS (R Data Structure). It’s a binary format, which means it represents data in a way that’s directly readable by computers but not easily readable by humans. The primary advantage of binary formats, like RDS, is they often allow faster read and write operations and can maintain all the intricacies of data structures. This ensures that when an R object is saved in RDS format and then reloaded, its structure and metadata remain unaltered.

To save an R object as an RDS file, use the saveRDS() function.

# Create folder for exported files

dir.create(path = "exported-files", showWarnings = FALSE)

# Save btcusd data as RDS file

saveRDS(object = btcusd, file = "exported-files/btcusd.rds")In this example:

objectrepresents the R object to be saved.fileindicates the path and filename where the data will be stored or overwritten.

To retrieve the object from the RDS file into R, use the readRDS() function.

# Load btcusd data from an RDS file

btcusd_loaded <- readRDS(file = "exported-files/btcusd.rds")

identical(btcusd, btcusd_loaded)## [1] TRUEKey Points:

- Always check your working directory using

getwd()to ensure files are saved where intended. Adjust it withsetwd()if necessary. - Remember, RDS files are designed for R. While efficient for R-to-R data transfers, they might not be compatible with other software.

- Ensure your storage can accommodate the file size, especially for large datasets. Though RDS files are compressed, large datasets can still occupy significant space.

- Always exercise caution when loading RDS files from unknown sources, as they could contain harmful code.

Overall, RDS is a reliable choice for preserving R objects between sessions and projects.

DSV

For compatibility across various software applications, it’s often useful to save data as DSV files, instead of R-specific formats. The write.table() function facilitates the export of data frames to DSV formats, including CSV and TSV.

# Create folder for exported files

dir.create(path = "exported-files", showWarnings = FALSE)

# Export Bitcoin price data as TSV file

write.table(x = btcusd,

file = "exported-files/btcusd.tsv",

sep = "\t",

row.names = FALSE)Here:

xrepresents the data frame to export.filedenotes the desired path and filename for the DSV file.sepspecifies the delimiter between fields. In this case, we’re using a tab (\t) for a TSV file. Notably, usingwrite.csv()is akin towrite.table()withsep = ",".- With

row.names = FALSE, the exported file won’t include row names, which are typically just sequential numbers.

By tailoring the parameters of write.table(), you can effectively store your data in the preferred format.

Points to remember:

- Always verify the working directory with

getwd()to ensure the file is saved where intended. If necessary, adjust it usingsetwd(). - After exporting, open the file in a text editor or spreadsheet application to ensure its contents are as expected.

- Be patient with large datasets. Exporting might take time, so allow R to finish the process before exiting.

Here are alternative methods for exporting DSV files in R:

- The

write_delim()function from thereadrpackage, part of the Tidyverse, exports data frames to DSV format. This function is especially useful when working with tibbles. - The

fwrite()function from thedata.tablepackage is another option for exporting data frames to DSV files. This function is optimized for speed and efficiency. - For time series data, the

write.zoo()function from thezoopackage allows you to exportzooorxtsobjects directly as DSV files.

To fully understand the capabilities and unique features of these functions, it’s recommended to consult their respective documentation using ?write_delim, ?fwrite, and ?write.zoo after loading the readr, data.table, and zoo packages.

Note that DSV export doesn’t retain attributes and may misclassify data types on import:

# Import the exported TSV file

btcusd_loaded <- read.table(file = "exported-files/btcusd.tsv",

sep = "\t",

header = TRUE)

# Verify if the original and imported TSV files match

identical(btcusd, btcusd_loaded)## [1] FALSETherefore, while DSV files offer better software compatibility than RDS, they fall short in preserving all attributes and data types of the original object.

5.2 Process Stock and Oil Prices

This section offers a roadmap for acquiring, manipulating, visualizing, and analyzing financial data using R using stock and oil price data as example. This section begins by discussing Web APIs as a method for directly fetching data, circumventing manual downloads and uploads. The quantmod and Quandl packages are used to fetch data from various APIs.

Following data acquisition, the section guides the reader through merging disparate data streams—such as stock and commodity prices—into a unified dataset. With the data merged, it presents methods to visualize the time-series data using plotting functionalities tailored for xts objects. The focus then shifts to transforming this raw data into a more analytically amenable form, dealing specifically with the issues of irregular frequency and missing values to create a regular time series at a monthly frequency.

Finally, the section concludes by demonstrating how to tabulate key statistics like mean, volatility, and correlation. These statistics offer a quantitative lens through which to understand the dataset’s central tendencies, dispersion, and relational aspects. Altogether, the section provides a comprehensive workflow for handling financial data, from acquisition to data analysis.

5.2.1 Web API

If your computer is connected to the internet, you can directly fetch data within R, bypassing the need to download data files manually and then import them into R. This section explains how to download financial and economic data in R using a Web API.

An Application Programming Interface (API), specifically a Web API, is more than just a data file saved on a website. It is a set of rules, protocols, and tools that enable two software entities to communicate with each other. In the context of data retrieval, a Web API serves as an interface between web servers and clients, offering a systematic way to access data. When you query a Web API, the server typically generates a response dynamically based on the request parameters it receives. This data can come in various formats such as JSON, XML, HTML, or plain text.

In R, direct interaction with Web APIs is often unnecessary, thanks to specialized R packages that handle this task. These packages translate fetched data into familiar R formats like data frames or xts objects. For instance, the imfr package fetches data from the IMF API, while the OECD and Quandl packages fetch data from the OECD and Nasdaq APIs, respectively. General-purpose packages like quantmod can interact with multiple APIs. To find an API for a specific database, a simple Google search such as “r web api database_name” should suffice.

In this chapter, we utilize the getSymbols() function from the quantmod package and the Quandl() function from the Quandl package to fetch data directly into R.

5.2.2 Download via quantmod

The quantmod package by Ryan and Ulrich (2024a) serves as a comprehensive toolkit for quantitative finance, primarily focused on data acquisition, manipulation, and visualization. It is designed to assist in the workflow of both financial traders and researchers. One of the package’s key functions is getSymbols(), which allows for easy access to financial data from multiple sources like Yahoo Finance, Google Finance, and Federal Reserve Economic Data (FRED).

Using getSymbols(), you can fetch various types of financial data such as stock prices, trading volumes, and other market indicators. The function downloads the data and converts it into an xts object, a data structure introduced in Chapter 4.8 that is designed to hold time-ordered data.

Here’s a basic example of using getSymbols() to fetch stock data for Apple Inc:

# Load the quantmod package

library("quantmod")

# Download Apple stock prices from Yahoo Finance

AAPL_stock_price <- getSymbols(

Symbols = "AAPL",

src = "yahoo",

auto.assign = FALSE,

return.class = "xts")

# Display the most recent downloaded stock prices

tail(AAPL_stock_price)## AAPL.Open AAPL.High AAPL.Low AAPL.Close AAPL.Volume AAPL.Adjusted

## 2024-06-25 209.15 211.38 208.61 209.07 56713900 209.07

## 2024-06-26 211.50 214.86 210.64 213.25 66213200 213.25

## 2024-06-27 214.69 215.74 212.35 214.10 49772700 214.10

## 2024-06-28 215.77 216.07 210.30 210.62 82542700 210.62

## 2024-07-01 212.09 217.51 211.92 216.75 60402900 216.75

## 2024-07-02 216.15 220.38 215.10 220.27 57960500 220.27After running these commands, you’ll have the Apple stock data stored in an xts object, ready for your analysis and visualization tasks.

The arguments in this context are:

Symbols: Specifies the instrument to import. This could be a stock ticker symbol, exchange rate, economic data series, or any other identifier.auto.assign: When set to FALSE, data must be assigned to an object (here,AAPL_stock_price). If not set to FALSE, the data is automatically assigned to theSymbolsinput (in this case,AAPL).return.class: Determines the type of data object returned, e.g.,ts,zoo,xts, ortimeSeries.src: Denotes the data source from which the symbol originates. Some examples include “yahoo” for Yahoo Finance, “google” for Google Finance, “FRED” for Federal Reserve Economic Data, and “oanda” for Oanda foreign exchange rates.

To find the correct symbol for financial data from Yahoo Finance, visit finance.yahoo.com and search for the company of interest, e.g., Apple. The symbol is the series of letters inside parentheses. For example, for Apple Inc. (AAPL), use Symbols = "AAPL" (and src = "yahoo").

To download economic data from FRED, visit fred.stlouisfed.org, and search for the data series of interest, e.g., unemployment rate. Click on one of the suggested data series. The symbol is the series of letters inside parentheses. For example, for Unemployment Rate (UNRATE), use Symbols = "UNRATE" (and src = "FRED").

Note that Yahoo Finance provides data in OHLC format, consisting of six columns: AAPL.Open, AAPL.High, AAPL.Low, AAPL.Close, AAPL.Volume, and AAPL.Adjusted. These values represent the opening, highest, lowest, and closing prices for a given market day, the trade volume for that day, and the adjusted closing price, which accounts for stock splits. These columns can be accessed using quantmod’s Op(), Hi(), Lo(), Cl(), Vo(), and Ad() functions. Typically, the AAPL.Adjusted column is of most interest.

# Extract adjusted Apple share price

AAPL_stock_price_adj <- Ad(AAPL_stock_price)

# Display the most recent adjusted stock prices

tail(AAPL_stock_price_adj)## AAPL.Adjusted

## 2024-06-25 209.07

## 2024-06-26 213.25

## 2024-06-27 214.10

## 2024-06-28 210.62

## 2024-07-01 216.75

## 2024-07-02 220.275.2.3 Download via Quandl

Quandl is a data service that provides access to many financial and economic data sets from various providers. It has been acquired by Nasdaq Data Link and is now operating through the Nasdaq data website: data.nasdaq.com. Some data sets require a paid subscription, while others can be accessed for free. Quandl provides an API that allows you to import data from a wide variety of languages, including Excel, Python, and R. To fetch data into R, the Quandl() function from the Quandl package is employed.

To use Quandl, first get a free Nasdaq Data Link API key at data.nasdaq.com/sign-up. After that, install and load the Quandl package and provide the API key with the function Quandl.api_key():

# Load Quandl package

library("Quandl")

# Provide API key

api_quandl <- "CbtuSe8kyR_8qPgehZw3" # Replace this with your API key

Quandl.api_key(api_quandl)Then, you can download data using Quandl(), such as fetching oil price data:

# Download monthly crude oil prices from Nasdaq Data Link

# ODA_oil_price <- Quandl(code = "ODA/POILAPSP_USD", type = "xts")

ODA_oil_price <- Quandl(code = "BSE/SI1400", type = "xts")$Close

# Display the downloaded crude oil prices

tail(ODA_oil_price)## Close

## 2023-07-14 19064.63

## 2023-07-17 19137.22

## 2023-07-18 19159.95

## 2023-07-19 19268.31

## 2023-07-20 19370.52

## 2023-07-21 19373.83Here, the code argument refers to both the data source and the symbol in the format “source/symbol”. The type argument specifies the type of data object: data.frame, xts, zoo, ts, or timeSeries.

To find the correct code for the Quandl function, visit data.nasdaq.com, and search for the data series of interest (e.g., oil price). The code is the series of letters listed in the left column, structured like this: .../..., where ... are letters. For example, for the crude oil price provided by IMF’s Open Data for Africa (ODA), use code = "ODA/POILAPSP_USD".

ODA’s crude oil price data is monthly and does not include the most recent values. For more frequent and up-to-date data, go to the search results for “oil price” and look for the dataset from the Organization of the Petroleum Exporting Countries (OPEC). Its identifier, QDL/OPEC, isn’t immediately visible in the search listings. To locate it, click on the OPEC dataset link and find the code beneath the data table. To retrieve this data, use Quandl.datatable() instead of Quandl() since it’s structured as a data table, not a typical time series.

# Download daily crude oil prices from Nasdaq Data Link

OPEC_oil_price = Quandl.datatable("QDL/OPEC")

# Convert data frame to xts object

OPEC_oil_price = xts(x = OPEC_oil_price$value, order.by = OPEC_oil_price$date)

# Display the downloaded crude oil prices

tail(OPEC_oil_price)## [,1]

## 2024-01-18 79.39

## 2024-01-19 80.27

## 2024-01-22 79.70

## 2024-01-23 81.30

## 2024-01-24 81.05

## 2024-01-25 81.985.2.4 Clean Data

When data is retrieved using R packages that interact with Web APIs, the likelihood of encountering misassigned data types is minimal. This is in contrast to the often encountered type issues when importing from DSV or Excel files. Nonetheless, the retrieved data object may still need conversion to a more suitable data structure. For example, we converted the OPEC_oil_price object from a data frame to an xts object.

Storing meta-information, such as the data source and time of import, as contextual attributes can be particularly useful. Since the data is directly imported via R code, it’s possible to preserve the import command itself as an attribute for future reference or replication:

# Record the time of data import

attr(AAPL_stock_price, "time_of_import") <- Sys.time()

attr(AAPL_stock_price, "time_of_import")## [1] "2024-07-03 08:48:21 CDT"# Define the function used to import AAPL stock data

import_AAPL_data <- function() {

quantmod::getSymbols(

Symbols = "AAPL",

src = "yahoo",

auto.assign = FALSE,

return.class = "xts")

}

# Attach the import function as an attribute to the data object

attr(AAPL_stock_price, "import_command") <- import_AAPL_data

# Demonstrate re-import of the data using the saved attribute

tail(attr(AAPL_stock_price, "import_command")())## AAPL.Open AAPL.High AAPL.Low AAPL.Close AAPL.Volume AAPL.Adjusted

## 2024-06-25 209.15 211.38 208.61 209.07 56713900 209.07

## 2024-06-26 211.50 214.86 210.64 213.25 66213200 213.25

## 2024-06-27 214.69 215.74 212.35 214.10 49772700 214.10

## 2024-06-28 215.77 216.07 210.30 210.62 82542700 210.62

## 2024-07-01 212.09 217.51 211.92 216.75 60402900 216.75

## 2024-07-02 216.15 220.38 215.10 220.27 57960500 220.27By doing so, the data object becomes self-descriptive, facilitating easier data sharing and replication across different project stages or among collaborators.

Note that data is only available for roughly 252 days per year, as indicated by the table generated below:

##

## 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

## 251 253 252 252 252 250 252 252 252 252 251 251 252 253 252 251

## 2023 2024

## 250 126That’s because stock market data is only available on trading days, excluding weekends and holidays. The result is an irregular time series with gaps varying from one day to over a week. To achieve a regular time series, consider interpolation or aggregating to a lower frequency like monthly data. This process is detailed in a subsequent chapter (see Chapter 5.2.8) and is also discussed in Chapters 4.8.

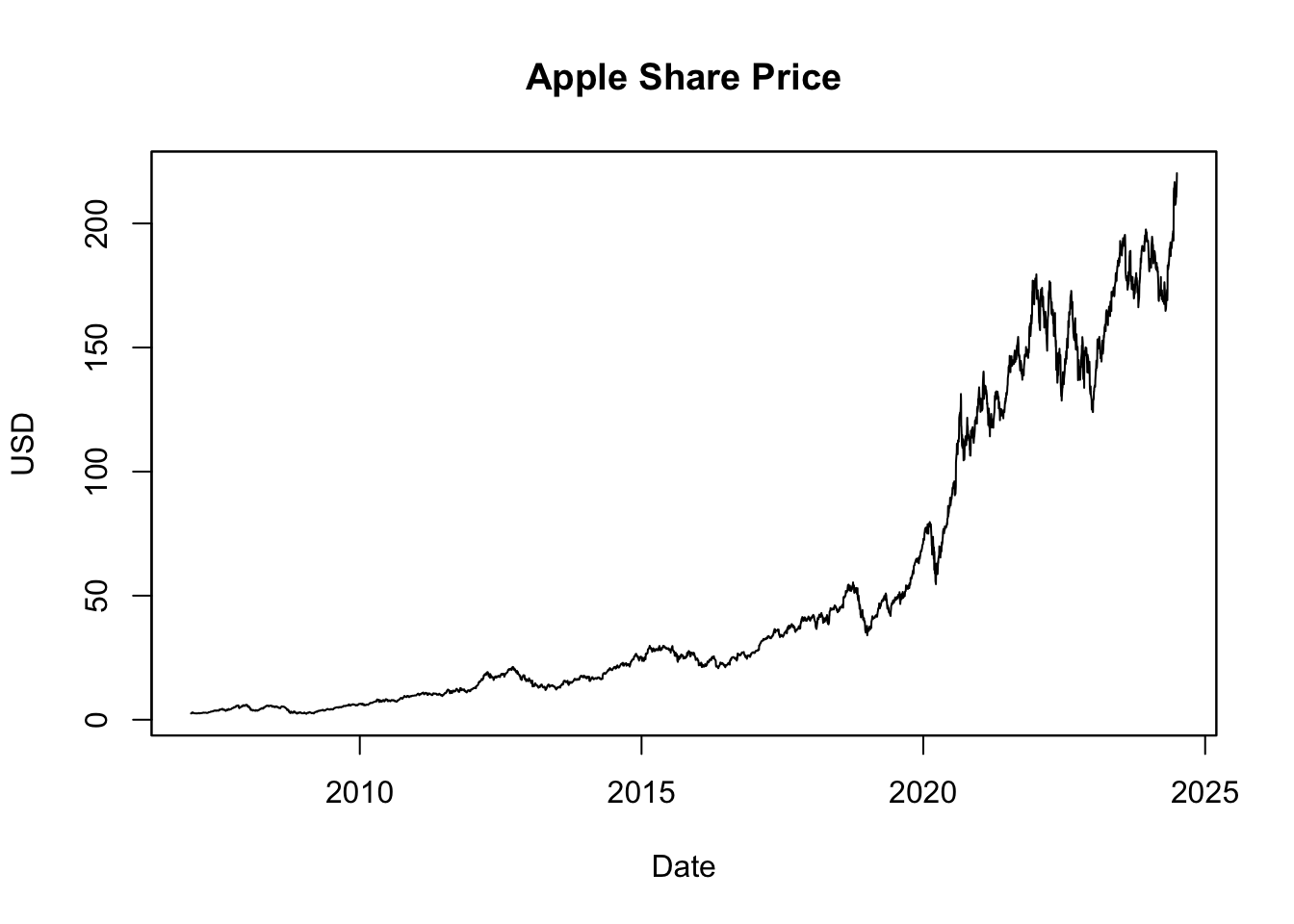

5.2.5 Plot Apple Stock Prices

Let’s visualize the Apple stock prices using the plot() function:

Figure 5.2: Apple Share Price

Observe that this plot differs from those created in previous chapters where data was stored as vectors - specifically, columns from data frames or tibbles. This variation occurs because plot() is a wrapper function, adapting its behavior to the object type supplied (see Chapter 3.5.11 for more on wrapper functions). When given an xts object, plot() defaults to using the plot.xts() method, optimized for visualizing time series data. Therefore, it’s no longer necessary to specify it as a line plot (type = "l"), as most time series are visualized with lines. To explicitly use the xts type plot() function, you can use the plot.xts() function, which behaves identically as long as the input object is an xts object. If not, the function will attempt to convert the object first.

As we’ve explored in Chapter 4.8, an xts object is an enhancement of the zoo object, offering more features. My personal preference leans towards the zoo variant of plot(), plot.zoo(), over plot.xts() because it operates more similarly to how plot() does when applied to data frames. To utilize plot.zoo(), apply it to the xts object like so:

# Plot adjusted Apple share price using plot.zoo()

plot.zoo(AAPL_stock_price_adj,

main = "Apple Share Price",

xlab = "Date", ylab = "USD")In this context, the inputs are as follows:

AAPL_stock_price_adjis thextsobject containing Apple Inc.’s adjusted stock prices, compatible withplot.zoo()thanks toxts’s extension ofzoo.mainsets the plot’s title, in this case, “Apple Share Price”.xlabandylabrespectively label the x-axis as “Date” and the y-axis as “USD”, denoting stock prices in U.S. dollars.

The usage of plot.zoo() provides a more intuitive plotting method for some users, replicating plot()’s behavior with data frames more closely compared to plot.xts().

Figure 5.3: Apple Share Price Visualized with plot.zoo()

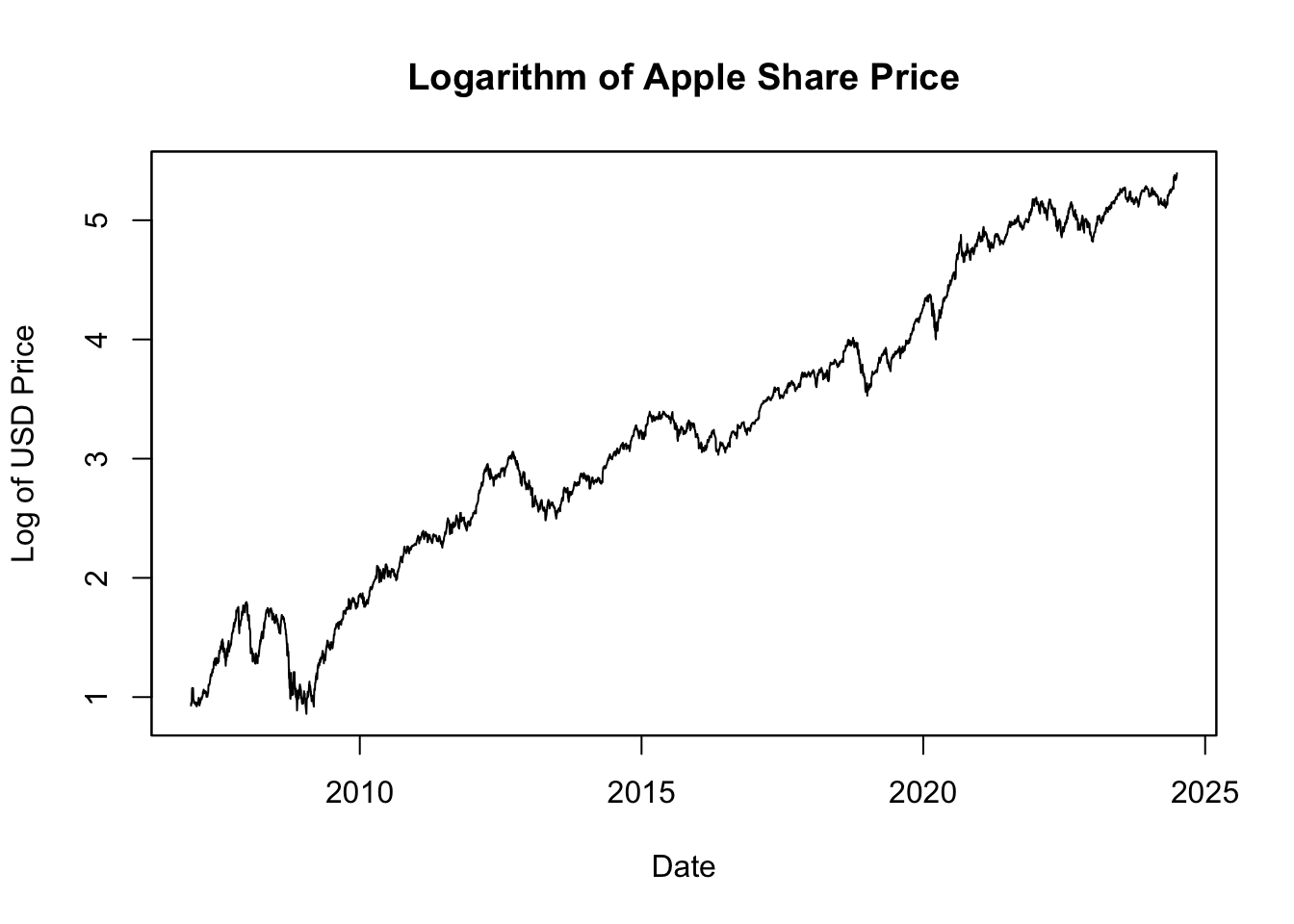

The resulting plot, shown in Figure 5.3, visualizes the Apple share prices over the last two decades. Stock prices often exhibit exponential growth over time, meaning the value increases at a rate proportional to its current value. As such, even large percentage changes early in a stock’s history may appear minor due to a lower initial price. Conversely, smaller percentage changes at later stages can seem more significant due to a higher price level. This perspective can distort the perception of a stock’s historical volatility, making past changes appear smaller than they were. To more accurately represent these proportionate changes, many analysts prefer using logarithmic scales when visualizing stock price data:

# Compute the natural logarithm (log) of Apple share price

log_AAPL_stock_price_adj <- log(AAPL_stock_price_adj)

# Plot log share price

plot.zoo(log_AAPL_stock_price_adj,

main = "Logarithm of Apple Share Price",

xlab = "Date", ylab = "Log of USD Price")

Figure 5.4: Logarithm of Apple Share Price

Figure 5.4 displays the natural logarithm of the Apple share prices. This transformation is beneficial because it linearizes the exponential growth in the stock prices, with the slope of the line corresponding to the rate of growth. More importantly, changes in the logarithm of the price correspond directly to percentage changes in the price itself. For example, if the log price increases by 0.01, this equates to a 1% increase in the original price. This property allows for a direct comparison of price changes over time, making it easier to interpret and understand the magnitude of these changes in terms of relative growth or decline.

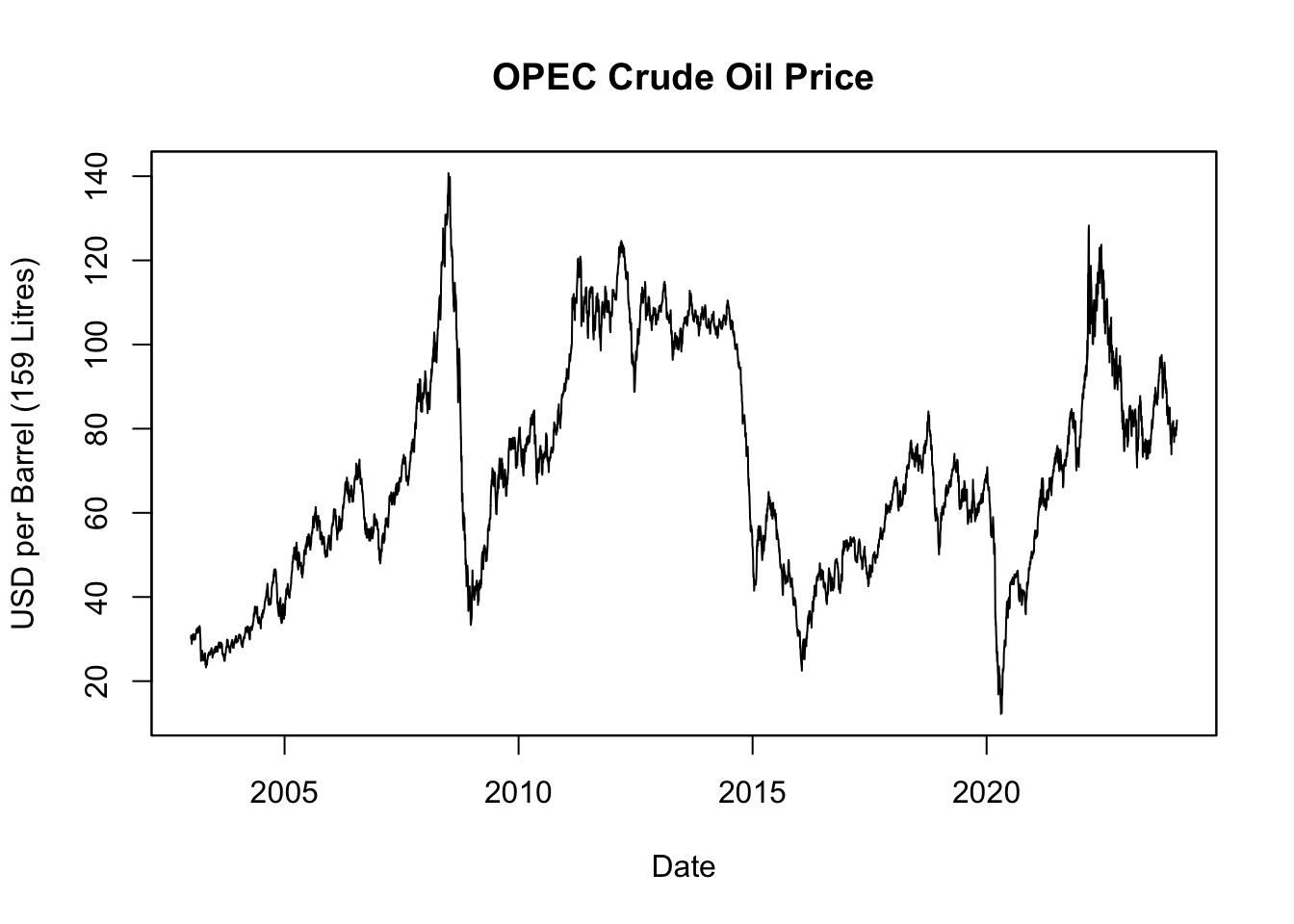

5.2.6 Plot Crude Oil Prices

Now, we’ll use the plot.zoo() function to graph the crude oil price:

# Plot crude oil prices

plot.zoo(OPEC_oil_price,

main = "OPEC Crude Oil Price",

xlab = "Date",

ylab = "USD per Barrel (159 Litres)")

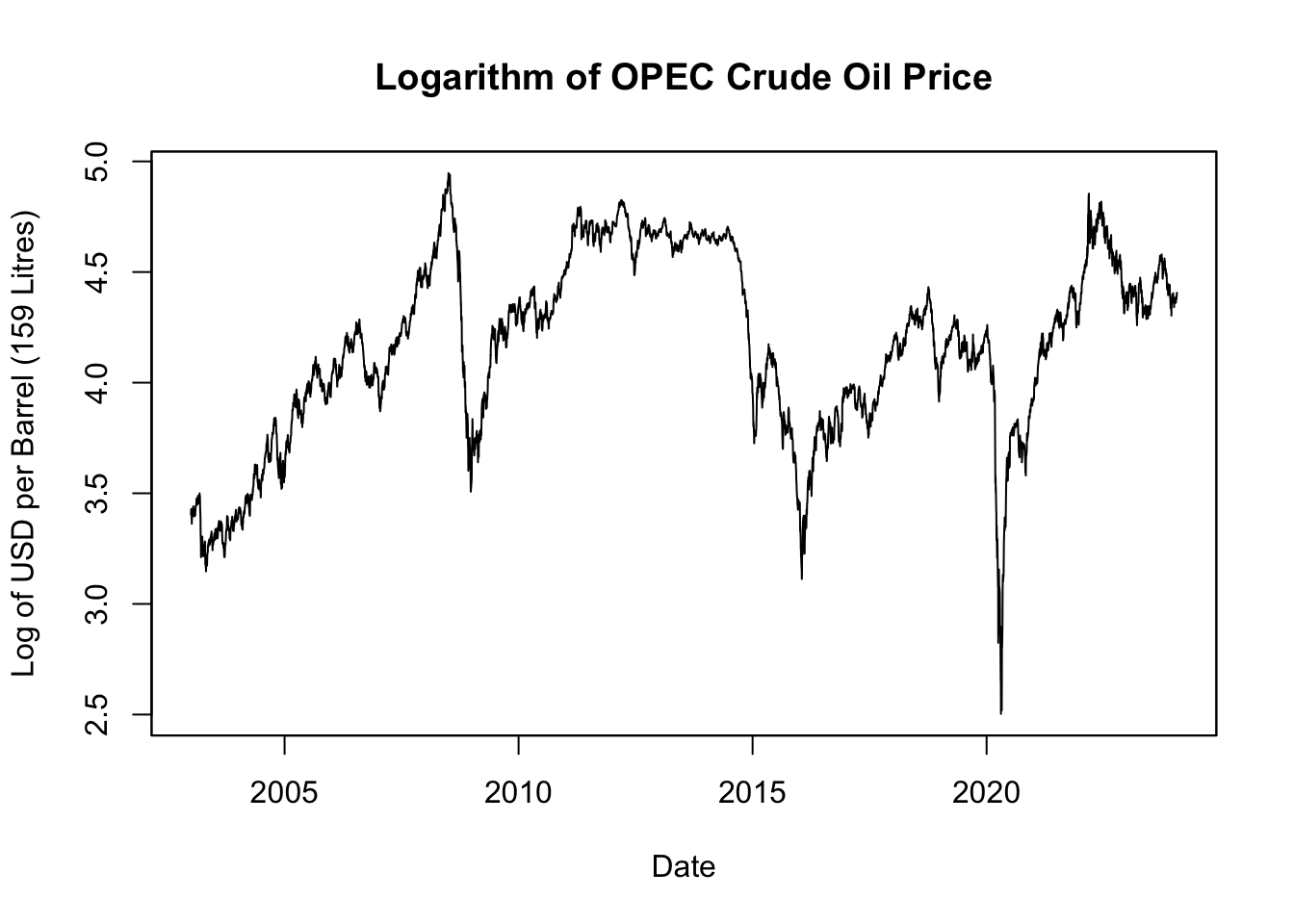

Figure 5.5: OPEC Crude Oil Price

Figure 5.5 displays the OPEC crude oil prices over the last two decades. While stock prices often exhibit long-term exponential growth due to company expansions and increasing profits, oil prices don’t inherently follow the same pattern. The primary drivers of oil prices are supply and demand dynamics, shaped by a myriad of factors such as geopolitical events, production changes, advancements in technology, environmental policies, and shifts in global economic conditions. Oil prices, as a result, can undergo substantial fluctuations, exhibiting high volatility with periods of significant booms and busts, rather than consistent exponential growth.

Visualizing oil prices over time can benefit from the use of a logarithmic scale:

# Compute the natural logarithm (log) of crude oil prices

log_OPEC_oil_price <- log(OPEC_oil_price)

# Plot log crude oil prices

plot.zoo(log_OPEC_oil_price,

main = "Logarithm of OPEC Crude Oil Price",

xlab = "Date",

ylab = "Log of USD per Barrel (159 Litres)")

Figure 5.6: Logarithm of OPEC Crude Oil Price

The natural logarithm of crude oil price, depicted in Figure 5.6, offers a clearer view of relative changes over time. It does this by rescaling the data such that equivalent percentage changes align to the same distance on the scale, regardless of the actual price level at which they occur. This transformation means a change in the log value can be read directly as a percentage change in price. So, a decrease of 0.01 in the log price corresponds to a 1% decrease in the actual price, whether the initial price was $10, $100, or any other value. This makes the data more intuitive and straightforward to interpret, particularly when tracking price trends and volatility across various periods.

5.2.7 Merge Data

In this section, we focus on merging and cleaning two time-series datasets: Apple’s adjusted stock price (AAPL_stock_price_adj) and OPEC’s oil price (OPEC_oil_price). We’ll use R’s merge() function to combine these series into a single data object for comparative analysis.

## AAPL.Adjusted OPEC_oil_price

## 2003-01-02 NA 30.05

## 2003-01-03 NA 30.83

## 2003-01-06 NA 30.71Note that merging AAPL_stock_price_adj and OPEC_oil_price does not require a by argument because both datasets are xts objects. In the case of xts, merging is done automatically by date index via the merge.xts() method.

After merging, it’s sometimes useful to trim rows with NA values at either end, as they could affect subsequent analysis. The function na.trim() serves this purpose.

## AAPL.Adjusted OPEC_oil_price

## 2007-01-03 2.530319 55.42

## 2007-01-04 2.586482 53.26

## 2007-01-05 2.568063 51.30It’s also informative to examine specific periods where data is missing for either series. For instance, we can focus on the year 2022 to identify such instances.

## AAPL.Adjusted OPEC_oil_price## AAPL.Adjusted OPEC_oil_price

## 2022-01-17 NA 86.38

## 2022-02-21 NA 94.04

## 2022-05-30 NA 120.01

## 2022-06-20 NA 113.39

## 2022-07-04 NA 115.25

## 2022-09-05 NA 99.76

## 2022-11-24 NA 81.52While OPEC oil prices are globally traded and thus consistently available, AAPL stock prices have gaps due to U.S. market holidays, which are listed in Table 5.2 below.

Date | U.S.-Specific Holiday |

|---|---|

2022-01-17 | Martin Luther King Jr. Day |

2022-02-21 | Presidents' Day |

2022-05-30 | Memorial Day |

2022-06-20 | Juneteenth |

2022-07-04 | Independence Day |

2022-09-05 | Labor Day |

2022-11-24 | Thanksgiving |

Recognizing these details is important for time-series analysis.

5.2.8 Transform Data

In this section, we undertake a series of data transformations to prepare for further analysis. These transformations include the removal of missing values, aggregation to a monthly frequency, and computation of stock returns.

Return Formula

Returns on stocks or commodities are defined as the percentage change in price, given by: \[ r_t = 100 \left( \frac{P_t - P_{t-1}}{P_{t-1}} \right) \% \approx 100 \left( \ln P_t - \ln P_{t-1} \right)\% \] Here, \(\ln P_t\) is the natural logarithm of \(P_t\). The log difference, \(\ln P_t - \ln P_{t-1}\), approximates the arithmetic return, \(\frac{P_t - P_{t-1}}{P_{t-1}}\), particularly for small returns (less than \(\pm 20\%\)).

Log returns are better for understanding how money grows over time. Imagine you invest $100 in a stock. On the first day, the stock gains 50%, so your investment is now worth $150. The next day, the stock loses 33.33%, bringing your investment down to $100 again.

Using arithmetic returns:

- First day: (150 - 100) / 100 = 0.5 or 50%

- Second day: (100 - 150) / 150 = -0.3333 or -33.33%

- Total return = 50% - 33.33% = 16.67%

If you simply sum the arithmetic returns, you’d think you have a positive total return of 16.67%. But you’re right back where you started, with $100.

Using log returns:

- First day: \(\ln\)(150/100) = 0.4055 or 40.55%

- Second day: \(\ln\)(100/150) = -0.4055 or -40.55%

- Total log return = 40.55% - 40.55% = 0.00%

The total log return correctly shows that, over the two days, you haven’t gained or lost any money.

This example illustrates why log returns can be less misleading when you are making multiple trades or assessing performance over time. They better capture the compounding effect and provide a more accurate representation of your returns.

Aggregate to Regular Frequency

We previously noted that stock and commodity prices have irregular frequencies, with approximately 252 trading days per year. Consequently, the notion of “return” can vary in duration, from one day to an entire week, which can introduce inconsistencies in the analysis.

To address this, one approach is to interpolate the data to a daily frequency for 365 days a year. Another approach is to aggregate the data to a less frequent, but more consistent, time frame like monthly, quarterly, or yearly periods. We opt for monthly aggregation. While a month is not a regular time unit—varying from 28 to 31 days - the variation in time intervals is considerably less problematic than in the original dataset.

It’s also important to note that U.S. stock market data are unavailable on U.S.-specific holidays, whereas commodity price data might still be accessible. To facilitate an apples-to-apples comparison between the two series, it’s crucial to eliminate the commodity prices for these particular days, as well. This can be accomplished using the na.omit() function on the merged dataset, which removes any rows where at least one column has missing data.

The apply.monthly() function from the xts package is used to convert the data from a daily to a monthly frequency. Specifically, the last available price within each month is used for the monthly aggregation. This method is consistent with how the adjusted stock prices were aggregated to a daily frequency using each day’s closing price.

This results in a time series with a consistent monthly frequency.

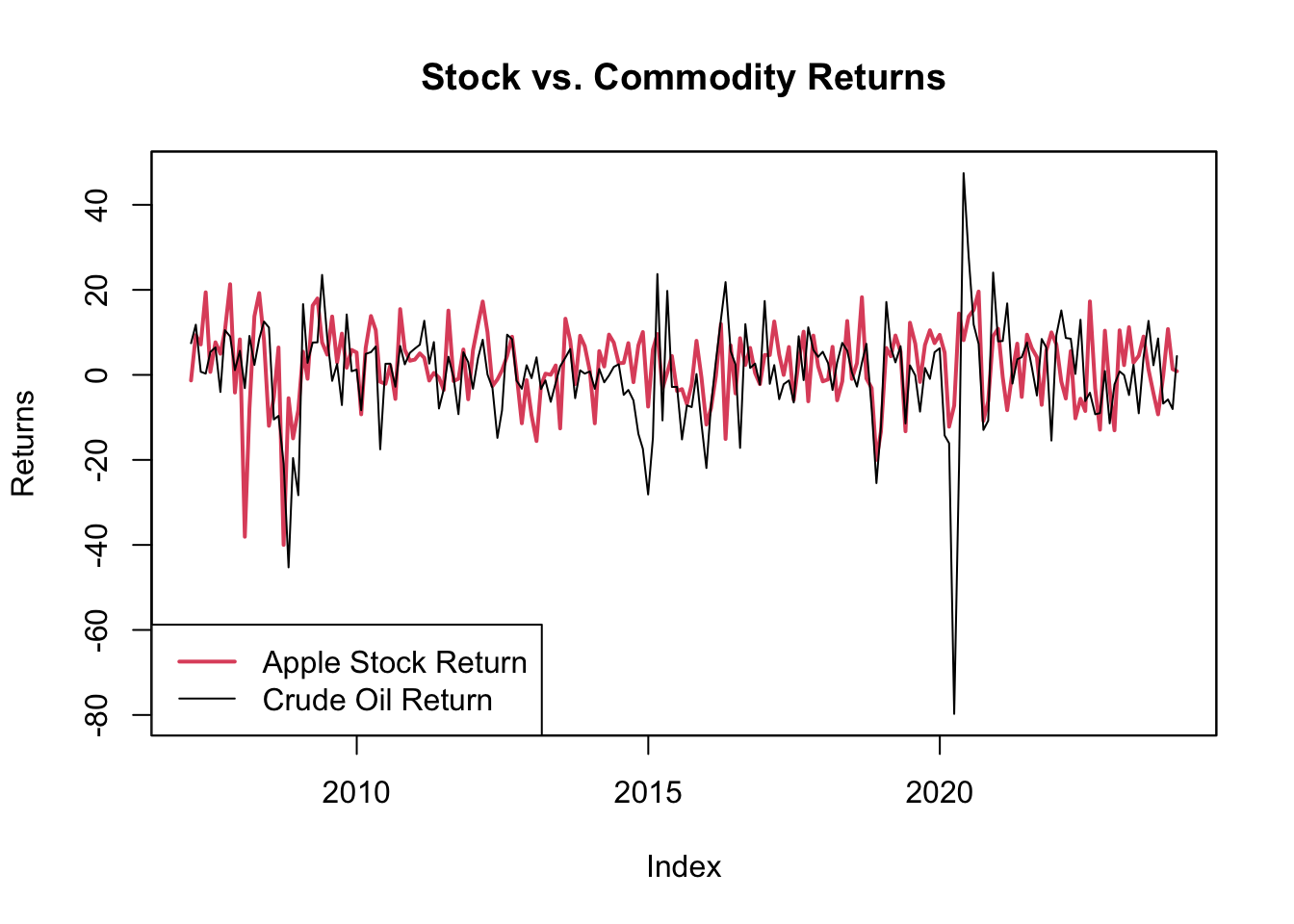

Compute Returns

Next, we calculate monthly returns using the log formula:

To visualize the returns of both assets on a single graph, use the plot.type = "single" argument within the plot.zoo() function.

# Plot returns

plot.zoo(Returns, plot.type = "single", main = "Stock vs. Commodity Returns",

col = c(2, 1), lwd = c(2, 1))

legend("bottomleft", legend = c("Apple Stock Return", "Crude Oil Return"),

col = c(2, 1), lwd = c(2, 1))

Figure 5.7: Stock vs. Commodity Returns

The plot, seen in Figure 5.7, reveals substantial volatility in both investment avenues. Apple’s stock appears less volatile than oil, which is counterintuitive given that Apple is subject to company-specific risks, whereas oil is a globally traded commodity.

While Apple’s stock is susceptible to company-specific risks such as earnings reports, innovation cycles, and market competition, its diversification in various products and global markets may cushion it against extreme volatility.

Oil, on the other hand, faces a unique blend of risks that contribute to its high volatility. These include geopolitical tensions, supply-demand imbalances, and external shocks such as natural disasters affecting production. Oil prices are also influenced by decisions made by major producers like OPEC, and global events that affect oil consumption. These multiple and often unpredictable factors can lead to large price swings in a short period, making oil a more volatile investment compared to a single company’s stock like Apple.

5.2.9 Tabulate Key Statistics

While visualizations offer a broad overview of trends and patterns, precise statistics are crucial for in-depth data analysis.

We will calculate key statistics such as the mean, volatility, minimum, and maximum returns. These measures provide insights into the central tendency and dispersion of the data. Additionally, we’ll compute correlation to examine how the two series move together and autocorrelation to understand the persistence of each series.

# Assemble key statistics in a data frame

stats_df <- rbind(

"Mean" = apply(Returns, 2, mean),

"Volatility (Standard Deviation)" = apply(Returns, 2, sd),

"Minimum Return" = apply(Returns, 2, min),

"Maximum Return" = apply(Returns, 2, max),

"Autocorrelation" = apply(Returns, 2, function(x) cor(x, lag.xts(x, 1),

use = "complete.obs")),

"Correlation to Crude Oil Return" = cor(Returns)[2, ])

colnames(stats_df) <- c("Apple Stock Return", "Crude Oil Return")

print(stats_df)## Apple Stock Return Crude Oil Return

## Mean 2.1151903 0.2173427

## Volatility (Standard Deviation) 9.0237222 11.9508115

## Minimum Return -39.9818045 -79.7423517

## Maximum Return 21.3255863 47.4494913

## Autocorrelation 0.1069703 0.3068170

## Correlation to Crude Oil Return 0.3273161 1.0000000The table title should specify the unit of return (in percent), the data frequency (monthly), and the time range for which the statistics are calculated.

# Define the time range for the statistics

time_interval <- format(x = range(index(Returns)), format = "%b %Y")

print(time_interval)## [1] "Feb 2007" "Jan 2024"# Create table title

stats_title <- paste("Monthly $\\%$-Return Statistics:",

paste(time_interval, collapse = " to "))

print(stats_title)## [1] "Monthly $\\%$-Return Statistics: Feb 2007 to Jan 2024"The table output from print(stats_df) is unsuitable for professional documents. For Microsoft Word or PowerPoint, export the table to a CSV file using write.table() and then insert it into the document. For LaTeX or HTML formats, employ the kable() function from the knitr package for a more refined table presentation.

# Load knitr for table rendering

library("knitr")

# Format table with rounded statistics

kable(x = round(stats_df, 2),

caption = stats_title,

format = "simple")

Table: (\#tab:return-stats) Monthly $\%$-Return Statistics: Feb 2007 to Jan 2024

Apple Stock Return Crude Oil Return

-------------------------------- ------------------- -----------------

Mean 2.12 0.22

Volatility (Standard Deviation) 9.02 11.95

Minimum Return -39.98 -79.74

Maximum Return 21.33 47.45

Autocorrelation 0.11 0.31

Correlation to Crude Oil Return 0.33 1.00In HTML or LaTeX documents, kable() produces neatly formatted tables, as seen in Table 5.3, by setting the format parameter to either format = "html" or format = "latex". For further customization options of the kable() function, refer to Chapter 6.7.

| Apple Stock Return | Crude Oil Return | |

|---|---|---|

| Mean | 2.12 | 0.22 |

| Volatility (Standard Deviation) | 9.02 | 11.95 |

| Minimum Return | -39.98 | -79.74 |

| Maximum Return | 21.33 | 47.45 |

| Autocorrelation | 0.11 | 0.31 |

| Correlation to Crude Oil Return | 0.33 | 1.00 |

Table 5.3 presents key statistical metrics for two investment avenues - Apple stock and crude oil - over a specific time period. Apple stock shows a mean return of approximately 2.12%, which is higher than crude oil’s mean return of 0.22%, suggesting better average performance. Moreover, crude oil exhibits greater volatility, with a standard deviation of about 11.95% compared to Apple’s 9.02%, indicating higher risk. Both investment avenues have experienced substantial downside risks, as evidenced by their minimum monthly returns of approximately -39.98% and -79.74% for Apple and crude oil, respectively. Crude oil has seen peaks of considerably higher returns than Apple, with a maximum of about 47.45%, compared to Apple’s 21.33%. The autocorrelation values of 0.11 for Apple and 0.31 for crude oil suggest that past returns have some, albeit limited, influence on future returns, more so for crude oil. Lastly, a correlation of 0.33 between Apple and crude oil returns indicates a mild positive relationship, implying that diversifying across these two asset classes may offer limited but non-negligible benefits.

5.2.10 Visualize Correlations

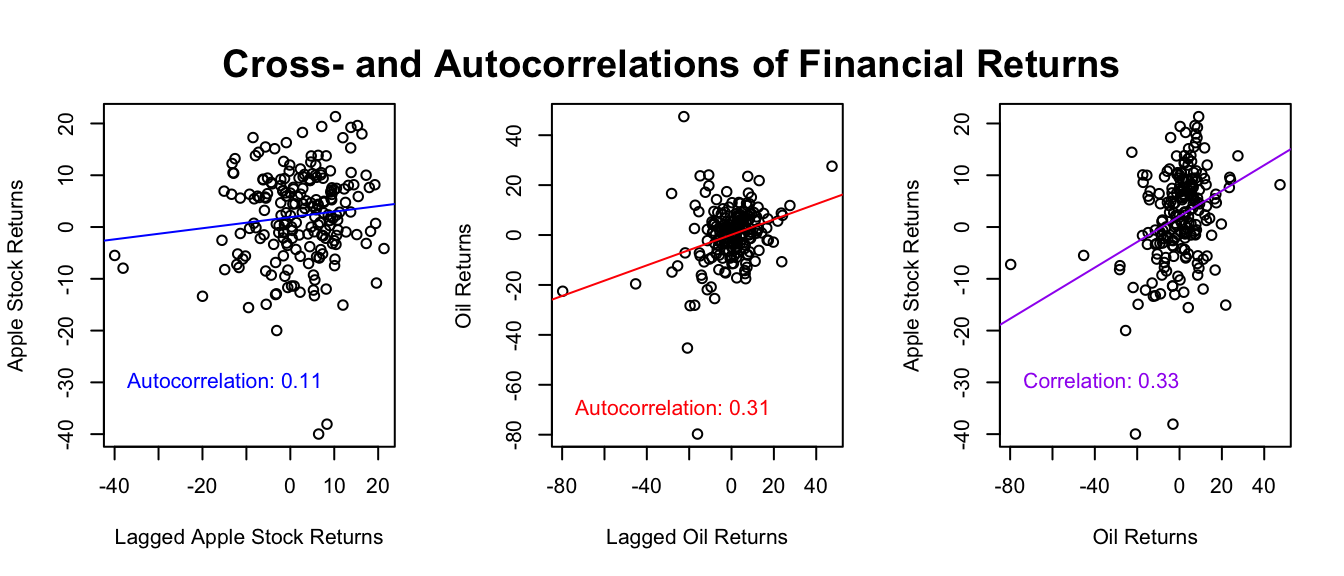

The correlations outlined in Table 5.3 merit further inspection through scatter plots. These visualizations allow for an assessment of whether the observed correlations hold broadly or are mainly driven by outliers.

# Put three plots on one figure

par(mfrow = c(1, 3))

# Autocorrelation of Apple returns and their lags

x_var <- lag.xts(Returns$AAPL.Adjusted, 1)

y_var <- Returns$AAPL.Adjusted

plot.default(x = x_var, y = y_var,

xlab = "Lagged Apple Stock Returns", ylab = "Apple Stock Returns")

abline(a = lm(y_var ~ x_var), col = "blue")

corr_text <- round(x = cor(x = x_var, y = y_var, use="complete.obs"), digits = 2)

text(x = min(na.omit(x_var)), y = min(na.omit(y_var)) + 10,

labels = paste("Autocorrelation:", corr_text), pos = 4, col = "blue")

# Autocorrelation of oil returns and their lags

x_var <- lag.xts(Returns$OPEC_oil_price, 1)

y_var <- Returns$OPEC_oil_price

plot.default(x = x_var, y = y_var,

xlab = "Lagged Oil Returns", ylab = "Oil Returns")

abline(a = lm(y_var ~ x_var), col = "red")

corr_text <- round(x = cor(x = x_var, y = y_var, use="complete.obs"), digits = 2)

text(x = min(na.omit(x_var)), y = min(na.omit(y_var)) + 10,

labels = paste("Autocorrelation:", corr_text), pos = 4, col = "red")

# Correlation of Apple and oil returns

x_var <- Returns$OPEC_oil_price

y_var <- Returns$AAPL.Adjusted

plot.default(x = x_var, y = y_var,

xlab = "Oil Returns", ylab = "Apple Stock Returns")

abline(a = lm(y_var ~ x_var), col = "purple")

corr_text <- round(x = cor(x = x_var, y = y_var, use="complete.obs"), digits = 2)

text(x = min(na.omit(x_var)), y = min(na.omit(y_var)) + 10,

labels = paste("Correlation:", corr_text), pos = 4, col = "purple")

# Add a title above all three plots

par(mfrow = c(1, 1)) # Reset to a single plot layout

title("Cross- and Autocorrelations of Financial Returns", outer = TRUE, line = -2)

Figure 5.8: Cross- and Autocorrelations of Financial Returns

In this R code:

par(mfrow = c(1, 3)): Configures the plotting space to display three plots in one row. The parametermfrowsets this layout, where the first number1specifies the number of rows and the second3specifies the number of columns.plot.default(...): Creates the scatter plots to compare returns. Theplot.default()function is invoked explicitly to bypass the default time-series plotting behavior ofxtsobjects that would be triggered by the genericplot()function. For a discussion on wrapper functions likeplot()and their associated methods, refer to Chapter 3.5.11.abline(lm(...), ...): Adds a line to the plot, showing the best-fit straight line through the data points. This line helps to visualize the relationship between the variables.corr_text <- round(cor(x, y, use = "complete.obs), 2): Calculates the rounded correlation between the two sets of returns, omitting pairs withNAvalues viause = "complete.obs".text(x = min(na.omit(x_var)), min(y = na.omit(y_var)) + 10, ...): Places a label on each plot, showing the rounded correlation coefficient. The text appears close to the minimum values of the x and y axes to avoid overlap.par(mfrow = c(1, 1)): Reverts the plotting area to a single-frame layout, necessary for adding an overarching title.title("Cross- and Autocorrelations of Financial Returns", outer = TRUE, line = -2): Positions an overarching title above all subplots. Theouter = TRUEparameter ensures the title appears outside the individual plot areas, andline = -2adjusts its vertical positioning.

Figure 5.8 examines the relationships among Apple stock returns, oil price returns, and their respective lagged values. The first two panels show that data points significantly diverge from the fitted lines, suggesting that the autocorrelation values 0.11 and 0.31 are likely influenced by outliers rather than representing a consistent trend. The third panel, however, shows a more stable relationship between Apple and oil returns, which correlation value is 0.33. This suggests that low (or high) returns in one asset generally coincide with low (or high) returns in the other. This matches what we see in Figure 5.7, where if one asset goes up or down, the other usually does the same.

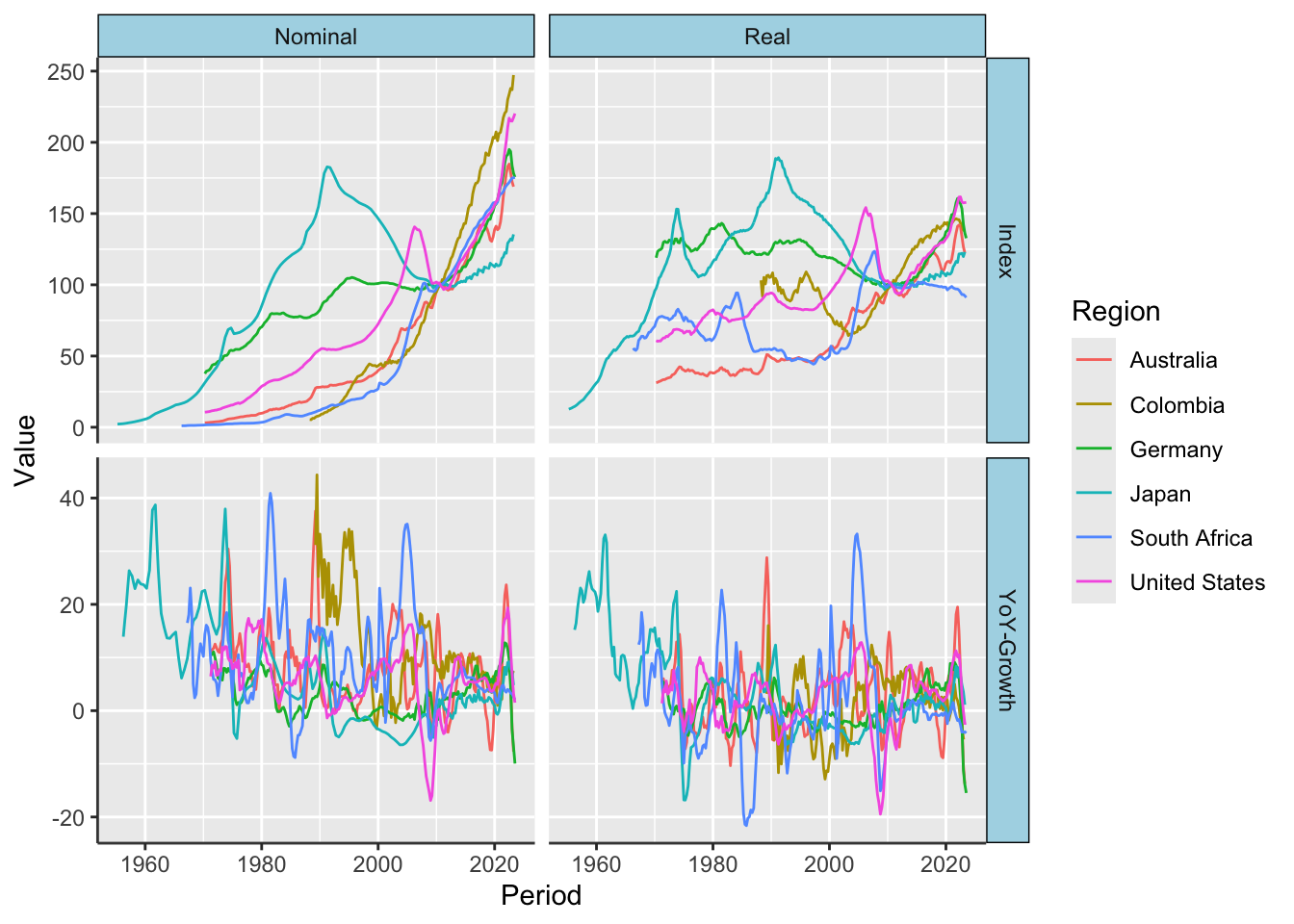

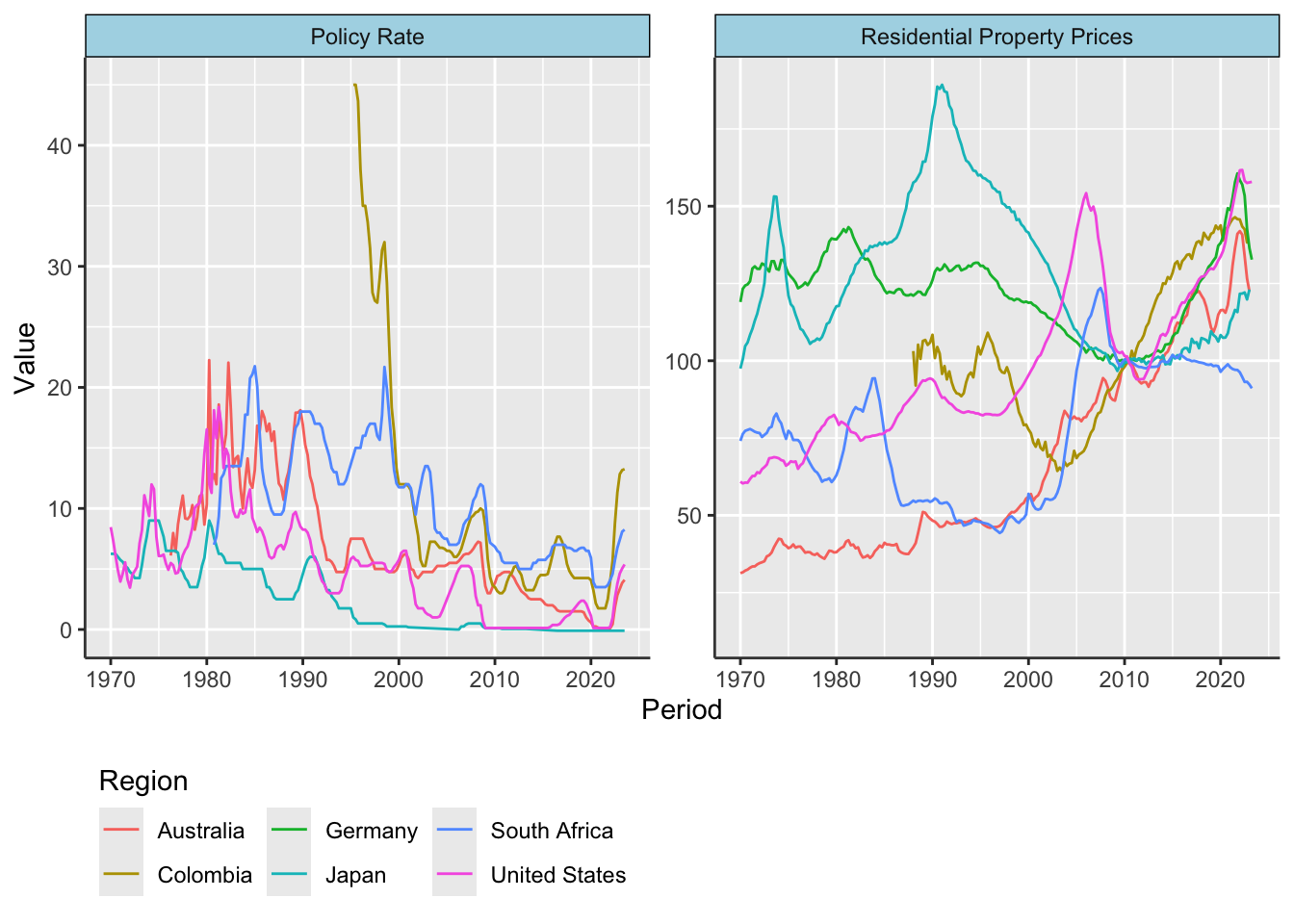

5.3 Process House Price Data

This chapter focuses on the processing of residential property price (RPP) data from the Bank for International Settlements (BIS, 2023b). The aim is to prepare the data for further analyses, especially its comparison with policy rates, also obtained from BIS (2023a). The chapter employs functions from the Tidyverse ecosystem in R, specifically using dplyr and tidyr for data manipulation as previously introduced in Chapter 4.6. Given the dataset’s multidimensional nature - spanning various indicators, regions, and time periods - the chapter introduces advanced plotting techniques via the ggplot2 package. It also addresses the complexities of computing associative statistics in such a multidimensional setting. Upon completing this chapter, readers will gain a holistic understanding of how to manage and analyze multidimensional data using these R tools.

5.3.1 Download Excel Workbook

To get RPP data from the BIS (2023b), follow these steps:

- Go to www.bis.org.

- Go to “Statistics” > “Property Prices” > “Selected Residential”.

- Click the “XLSX” button next to the data description: “Nominal and real residential property prices…”.

- Once downloaded, place the file in your R working directory, specifically in a folder named “files,” and name it

pp_selected.xlsx.

House prices will also be compared to policy rates from the BIS (2023a), obtained as follows:

- Go to www.bis.org.

- Go to “Statistics” > “Other Indicators” > “Policy Rates”.

- Click the “XLSX” button next to the data description: “Monthly data”.

- Once downloaded, place the file in your R working directory, specifically in a folder named “files,” and name it

cbpol.xlsx.

For guidance on finding and setting your working directory, see Chapters 3.7.1 and 3.7.2. To learn how to create a folder and download files directly from a website within R, check Chapter 3.7.3.

5.3.2 Import Excel Workbook

An Excel workbook (xlsx) is a file that contains one or more spreadsheets (worksheets), which are the separate “pages” or “tabs” within the file. An Excel worksheet, or simply a sheet, is a single spreadsheet within an Excel workbook. It consists of a grid of cells formed by intersecting rows (labeled by numbers) and columns (labeled by letters), which can hold data such as text, numbers, and formulas.

The readxl package by Wickham and Bryan (2023) provides functions that allow for importing Excel files into R as a tibble structure, which is the tidyverse-version of a data frame (see Chapter 4.6 for an overview on tibbles, and Chapter 3.6.7 for the tidyverse). Hence, to import the residential property price (RPP) database, which is an Excel workbook, install and load the readxl package by running install.packages("readxl") in the console and include the package at the beginning of your R script. You can then use the excel_sheets() function to print the names of all Excel worksheets in the workbook, and the read_excel() function to import a particular worksheet.

Here’s an illustration of how to employ the excel_sheets() function using the pp_selected.xlsx file downloaded from the Bank for International Settlements.

# Load the packages

library("readxl")

library("tibble")

library("dplyr")

library("tidyr")

# Get names of all Excel worksheets

sheet_names <- excel_sheets(path = "files/pp_selected.xlsx")

sheet_names## [1] "Content" "Summary Documentation" "Quarterly Series"This reveals that there are three Excel sheets: “Content”, “Summary Documentation”, and “Quarterly Series”. The “Content” sheet provides information about how the Excel workbook is structured, as well as how to cite the data when using it, and links to documentation files. The “Summary Documentation” sheet provides information about the house price variables, such as the variable’s code, reference area, unit of measurement, and whether it’s price adjusted. Finally, the “Quarterly Series” sheet stores the house prices, where each row is a different quarter, and each column is a different variable. There are four header rows, where the first three include information about the variable that is also available in the “Summary Documentation” sheet, and the last row references the variable’s code. Hence, it is sufficient to import “Summary Documentation” for variable information and “Quarterly Series” without the first three rows for the data.

# Import Excel worksheet: "Summary Documentation"

RPP_labels <- read_excel(

path = "files/pp_selected.xlsx",

sheet = "Summary Documentation",

col_names = TRUE, # The file has a header row with names

na = "-" # Character string representing NA values

)

# Import Excel worksheet: "Quarterly Series"

RPP_wide <- read_excel(

path = "files/pp_selected.xlsx",

sheet = "Quarterly Series",

col_names = TRUE, # The file has a header row with names

na = "", # Character string representing NA values

skip = 3 # Skips the first three rows

)As a side note, when the Excel workbook consists of a large number of sheets, e.g. each representing different variables, then it makes sense to use lapply() to import all sheets at once:

# Import all worksheets of an Excel workbook without customization

import_all <- lapply(sheet_names, function(x)

read_excel(path = "files/pp_selected.xlsx", sheet = x))

# Name the list elements, each representing a different worksheet

names(import_all) <- sheet_namesIn the provided code snippet, the lapply() function is used to apply the read_excel() function to each element in the sheet_names list, returning a list that is the same length as the input. Consequently, the import_all object becomes a list in which each element is a tibble corresponding to an individual Excel worksheet, which is named accordingly. For instance, to access the worksheet “Summary Documentation”, you would select import_all[["Summary Documentation"]]. This approach is useful if each sheet refers to a different variable, but in this case, since we only have three sheets, importing each sheet separately with sheet-specific customizations makes more sense.

5.3.3 Inspect and Clean Data

Once data is imported, a preliminary examination ensures its accuracy. Note that because read_excel() imports data as a tibble and not a data frame, R doesn’t print the entire data frame; hence, simply entering the data names RPP_labels and RPP into the console already provides a good overview. For more details, use RStudio’s spreadsheet-like viewer via View(RPP_labels) and View(RPP) (exclusive to RStudio and not included in R).

For a more detailed exploration of the data’s structure, execute str() or glimpse() from the tibble package, and execute summary() for a summary of the data.

## Rows: 248

## Columns: 9

## $ `Data set` <chr> "BIS_SPP", "BIS_SPP", "BIS_SPP", "BIS_SPP", "BIS_SPP"…

## $ Code <chr> "Q:4T:N:628", "Q:4T:N:771", "Q:4T:R:628", "Q:4T:R:771…

## $ Frequency <chr> "Quarterly", "Quarterly", "Quarterly", "Quarterly", "…

## $ `Reference area` <chr> "Emerging market economies (aggregate)", "Emerging ma…

## $ Value <chr> "Nominal", "Nominal", "Real", "Real", "Nominal", "Nom…

## $ Unit <chr> "Index, 2010 = 100", "Year-on-year changes, in per ce…

## $ Coverage <chr> "Emerging markets covered in the BIS residential prop…

## $ `Series title` <chr> "Residential property prices selected - Nominal - Ind…

## $ Breaks <chr> NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, N…Here, all variables of the RPP_labels tibble are of data type character <chr>, which makes sense, as they consist of verbal descriptions of the data.

Examining the data types of each column is crucial as they may be incorrectly assigned during import. Use sapply() in conjunction with class() to identify the types:

# Inspect the overall structure of the dataset

class(RPP_wide)

# Determine the class of each column

RPP_data_types <- sapply(RPP_wide, class)

# Validate if the first column 'Period' is of Date or POSIXct type

RPP_data_types[1]

# Confirm whether all remaining columns are numeric

all(RPP_data_types[-1] == "numeric")## [1] "tbl_df" "tbl" "data.frame"

## $Period

## [1] "POSIXct" "POSIXt"

##

## [1] TRUEIn this case, R correctly identifies the ‘Period’ as POSIXct and all house prices as numeric. No type conversions are needed.

To improve data clarity, consider adding contextual attributes like the data source and the count of imported rows, as we did with the imported Bitcoin price data in Chapter 5.1.4.

Lastly, pay attention to variable labels. The column Value in BIS’s RPP data indicates whether the residential property price (RPP) is "Real" or "Nominal". To avoid confusion with data values, the column name is changed to Measure. Additionally, the column Reference area is simplified to Region, and the Unit descriptions are abbreviated for ease. Converting these attributes into factors enhances computational efficiency.

# Rename variables

RPP_labels <- RPP_labels %>%

mutate(Code = factor(Code),

Region = factor(`Reference area`),

Unit = factor(Unit),

Measure = factor(Value))

# Abbreviate unit labels

renaming_vector <- c("Year-on-year changes, in per cent" = "YoY-Growth",

"Index, 2010 = 100" = "Index")

levels(RPP_labels$Unit) <- renaming_vector[levels(RPP_labels$Unit)]This R code performs two main tasks: renaming variables and modifying their labels.

- Rename Variables:

mutate(Code = factor(Code), Region = factor('Reference area'), Unit = factor(Unit), Measure = factor(Value)): Themutatefunction fromdplyris used to change the column names. Here,Reference areais renamed toRegionandValuetoMeasure. All these variables are also converted to factors which are more efficient for computation and analysis in R.

- Abbreviate Labels:

renaming_vector <- c("Year-on-year changes, in per cent" = "YoY-Growth", "Index, 2010 = 100" = "Index"): A vector calledrenaming_vectoris created to store the new abbreviated labels.levels(RPP_labels$Unit) <- renaming_vector[levels(RPP_labels$Unit)]: This line replaces the old labels in theUnitcolumn with the new abbreviated labels fromrenaming_vector.

The renaming is better done after converting to factors because R will then only change the factor levels instead of having to traverse through each string to replace it, thus enhancing computational efficiency.

5.3.4 Reshape Data

The process of reshaping data from wide to long format and vice versa is often critical for effective data analysis. For data frames, the reshape() function is commonly used, as explored in Chapter 4.5.8. For tibbles, we generally use pivot_longer() and pivot_wider() functions from the tidyr package. These are discussed in detail in Chapter 4.6.8.

From Wide to Long Format

Let’s take a look at the initial structure of our data. Tables 5.4 and 5.5 display our RPP data and its corresponding labels.

| Period | Q:US:R:628 | Q:US:R:771 | Q:XM:R:628 | Q:XM:R:771 |

|---|---|---|---|---|

| 2022-09-30 | 158.1889 | 2.7320 | 115.2157 | -2.4634 |

| 2022-12-31 | 157.5075 | -0.1327 | 110.6743 | -6.4343 |

| 2023-03-31 | 157.7020 | -2.4097 | 109.2423 | -7.1131 |

| Code | Region | Measure | Unit |

|---|---|---|---|

| Q:US:R:628 | United States | Real | Index |

| Q:US:R:771 | United States | Real | YoY-Growth |

| Q:XM:R:628 | Euro area | Real | Index |

| Q:XM:R:771 | Euro area | Real | YoY-Growth |

In Table 5.4, the data is organized in a wide format, where each variable forms a column. Conversely, Table 5.5 displays the labels in a long format, where each variable corresponds to a row. To align these two different structures, we employ the pivot_longer() function from the tidyr package.

# Load the necessary package

library("tidyr")

# Reshape the data from a wide to a long format.

RPP <- RPP_wide %>%

pivot_longer(cols = -Period,

names_to = "Code",

values_to = "Value",

values_drop_na = TRUE)The pivot_longer() function in the code reshapes the data from wide to long format. Here’s the breakdown of its arguments:

cols = -Period: Specifies that all columns except “Period” will be converted to a long format.names_to = "Code": The names of the reshaped columns will be stored in a new column named “Code”.values_to = "Value": The values from the reshaped columns will go into a new column named “Value”.values_drop_na = TRUE: Any rows that would containNAvalues in the new “Value” column are removed.

So, the function takes multiple columns and condenses them into two: one for the Code (original column names) and one for the Value (original data values), as is evident in Table 5.6.

| Period | Code | Value |

|---|---|---|

| 2022-09-30 | Q:US:R:628 | 158.1889 |

| 2022-09-30 | Q:US:R:771 | 2.7320 |

| 2022-09-30 | Q:XM:R:628 | 115.2157 |

| 2022-09-30 | Q:XM:R:771 | -2.4634 |

| 2022-12-31 | Q:US:R:628 | 157.5075 |

| 2022-12-31 | Q:US:R:771 | -0.1327 |

| 2022-12-31 | Q:XM:R:628 | 110.6743 |

| 2022-12-31 | Q:XM:R:771 | -6.4343 |

| 2023-03-31 | Q:US:R:628 | 157.7020 |

| 2023-03-31 | Q:US:R:771 | -2.4097 |

| 2023-03-31 | Q:XM:R:628 | 109.2423 |

| 2023-03-31 | Q:XM:R:771 | -7.1131 |

With the data now in long format, it becomes feasible to merge it with the labels. For this, we use the left_join() function from the dplyr package. This type of join is explained in Chapter 4.6.6. The advantage of a “left” join is that it ensures no data is omitted; if any labels are missing, the associated data remains intact, with the label fields populated as NA.

# Perform the merging operation

RPP <- RPP %>%

left_join(y = RPP_labels %>%

select(Code, Region, Unit, Measure),

by = "Code") %>%

select(-Value, everything(), Value)The left_join() function is used to merge two datasets based on a common column, in this case, “Code”.

y = RPP_labels %>% select(Code, Region, Unit, Measure): Specifies that the second dataset in the join is a subset ofRPP_labels, containing only the columns “Code”, “Region”, “Unit”, and “Measure,” omitting redundant or overly detailed columns like “Frequency” and “Coverage.”by = "Code": Specifies that the datasets will be merged based on the “Code” column.select(-Value, everything(), Value): Rearranges the columns, moving the “Value” column to the end.

The left_join() operation will keep all rows from RPP (the left dataset), and add corresponding data from RPP_labels where the “Code” matches. If there’s a “Code” in RPP that is not found in RPP_labels, that row will still be in the output, but the new columns (“Region”, “Unit”, “Measure”) will have NA values.

After merging, the data and labels appear fully integrated in a long format, as can be seen in Table 5.7.

| Period | Code | Region | Unit | Measure | Value |

|---|---|---|---|---|---|

| 2022-09-30 | Q:US:R:628 | United States | Index | Real | 158.1889 |

| 2022-09-30 | Q:US:R:771 | United States | YoY-Growth | Real | 2.7320 |

| 2022-09-30 | Q:XM:R:628 | Euro area | Index | Real | 115.2157 |

| 2022-09-30 | Q:XM:R:771 | Euro area | YoY-Growth | Real | -2.4634 |

| 2022-12-31 | Q:US:R:628 | United States | Index | Real | 157.5075 |

| 2022-12-31 | Q:US:R:771 | United States | YoY-Growth | Real | -0.1327 |

| 2022-12-31 | Q:XM:R:628 | Euro area | Index | Real | 110.6743 |

| 2022-12-31 | Q:XM:R:771 | Euro area | YoY-Growth | Real | -6.4343 |

| 2023-03-31 | Q:US:R:628 | United States | Index | Real | 157.7020 |

| 2023-03-31 | Q:US:R:771 | United States | YoY-Growth | Real | -2.4097 |

| 2023-03-31 | Q:XM:R:628 | Euro area | Index | Real | 109.2423 |

| 2023-03-31 | Q:XM:R:771 | Euro area | YoY-Growth | Real | -7.1131 |

The data in long format, showcased in Table 5.7, is often referred to as “tidy” data. This format makes it easier to work with the data in future analysis steps.

From Long to Wide Format

Some data manipulation tasks and R packages need data in a specific format. For example, the xts package for time series, as mentioned in Chapter 4.8, requires data in wide format. In this format, each row corresponds to a time period, and each column represents a variable.

The challenge in switching from long to wide format is that the long format has multiple descriptor columns, like Region, Unit, and Measure. In wide format, this results in complex column names, like Region.Unit.Measure, as displayed in the following Table ??.

| Period | Italy.Nominal.Index | Italy.Nominal.YoY-Growth | Italy.Real.Index |

|---|---|---|---|

| 2022-12-31 | 90.4318 | 2.6923 | 70.9075 |

| 2023-03-31 | 90.4318 | 1.0407 | 70.6296 |

| 2023-06-30 | 92.2100 | 0.7401 | 71.7172 |

The conversion from long to wide format, i.e. from Table 5.7 to 5.8, is achieved using the pivot_wider() function from the tidyr package.

# Reshape from long to wide

RPP_with_labels_wide <- RPP %>%

pivot_wider(id_cols = "Period",

names_from = c("Region", "Measure", "Unit"),

values_from = "Value",

names_sep = ".")In this R code snippet, the function pivot_wider() from the tidyr package is used to transform a long-format dataset (RPP) into a wide-format one (RPP_with_labels_wide). Here’s a breakdown of the function’s arguments:

id_cols = "Period": This sets the “Period” column as the identifier column, around which the reshaping will happen.names_from = c("Region", "Measure", "Unit"): The unique combinations of values in these columns (“Region,” “Measure,” “Unit”) will become new column names in the wide-format dataset.values_from = "Value": Specifies that the numerical “Value” column from the long-format dataset will be used to populate the cells in the new wide-format columns.names_sep = ".": The new column names generated from “Region,” “Measure,” and “Unit” will be separated by a period (.)

So the resulting RPP_with_labels_wide dataset, visualized in Table 5.8, will have a column for each unique combination of “Region,” “Measure,” and “Unit,” and these will be populated with the corresponding “Value” from the original RPP dataset. The “Period” column remains as the identifier.

The resulting wide-format data can be hard to read because of the complex column names. One solution is to filter and focus on specific subsets before converting to wide format. For instance, to focus on the real RPP index, we first filter the data:

# Select real RPP index

RPP_real_index <- RPP %>%

filter(Measure == "Real", Unit == "Index") %>%

select(Period, Region, `Real RPP` = Value)Then, we can convert this filtered data to wide format:

# Reshape from wide to long

RPP_real_index_wide <- RPP_real_index %>%

pivot_wider(id_cols = "Period",

names_from = c("Region"),

values_from = "Real RPP")Here, the column names become simpler, just representing different regions, as shown in Table 5.9. It makes the wide-format data easier to work with.

| Period | Australia | Colombia | Japan | Germany | South Africa | United States |

|---|---|---|---|---|---|---|

| 2022-09-30 | 133.8846 | 142.4936 | 122.0932 | 153.4093 | 93.1363 | 158.1889 |

| 2022-12-31 | 126.6149 | 138.2781 | 119.8312 | 142.6217 | 93.1787 | 157.5075 |

| 2023-03-31 | 122.4054 | 138.2344 | 123.0206 | 136.4207 | 92.2980 | 157.7020 |

By focusing on a subset, we simplify the wide-format data, making it more manageable for analysis.

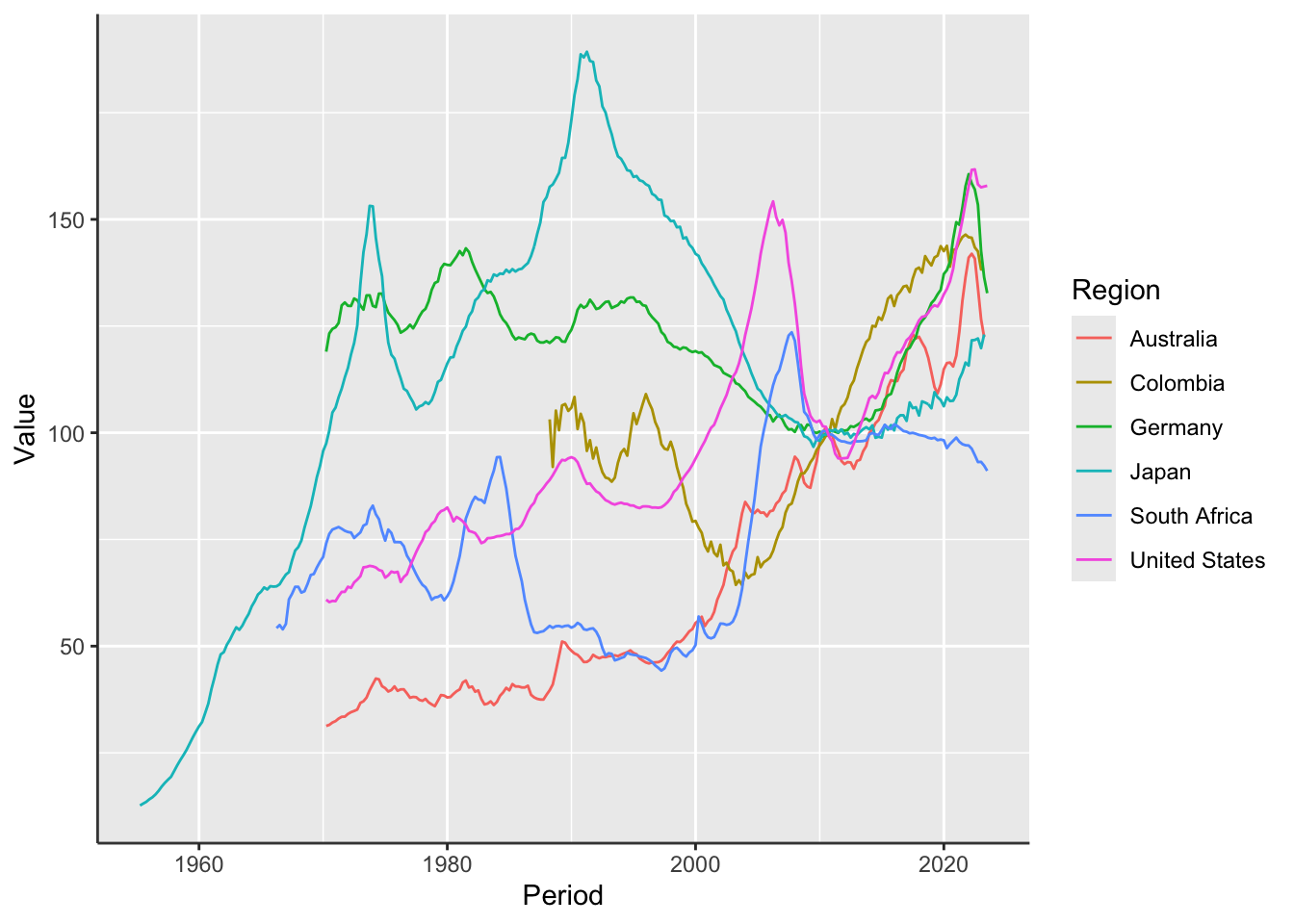

5.3.5 Layered Line Graphs

Line graphs serve to illustrate temporal trends and patterns. In R, there are two main approaches for creating such graphs: the base R plotting system, featuring functions like plot() and matplot(), and the ggplot2 package by Wickham et al. (2024), which employs the ggplot() function. Although both visualize data, there are stark differences in their approaches, particularly in their data format requirements, layering philosophies, and extensibility.

Basic Line Graphs Using matplot()

Base R functions like plot() and matplot() operate under a procedural paradigm. Essentially, what you see is what you get. Each function call adds or modifies specific attributes of the graph, and there’s limited scope for dynamically layering or extending the plot.

In the basic plot(x, y) function, a vector y is plotted relative to another vector x. When y is a matrix, matplot(x, y) serves as the alternative. Generally, matplot() anticipates data in wide format, where each time-series or category is allocated its own column. While this approach is convenient for simple visualizations, it may become cumbersome for more complex, multi-layered visualizations.

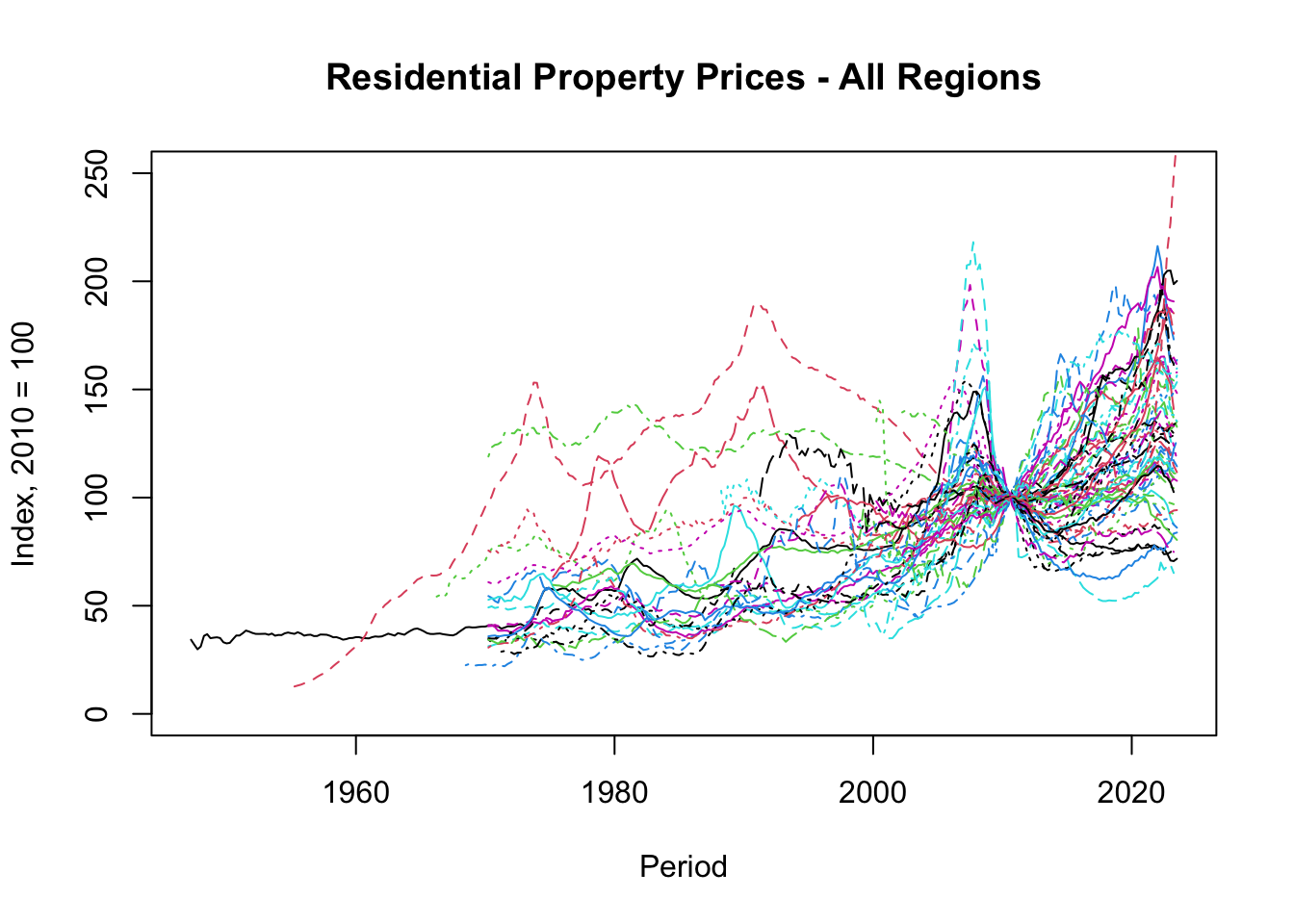

Here’s how to use matplot() to plot residential property prices for all regions, assuming the data is in wide format:

# Produce line plots

matplot(x = RPP_real_index_wide$Period,

y = RPP_real_index_wide[, -1],

type = "l",

main = "Residential Property Prices - All Regions",

xlab = "Period",

ylab = "Index, 2010 = 100",

ylim = c(0, 250))This R code chunk creates a line plot of residential property prices for all regions using the matplot() function. Here’s a breakdown of the code:

matplot(x = RPP_real_index_wide$Period, y = RPP_real_index_wide[, -1], type = "l"): The functionmatplot()is used to plot multiple lines. Thexargument specifies the time period to be plotted on the x-axis. Theyargument specifies the data for the y-axis, omitting the first column which contains the time period. Thetype = "l"argument indicates that lines should be used for the plot.main = "Residential Property Prices - All Regions": Sets the title of the graph.xlab = "Period": Labels the x-axis as “Period”.ylab = "Index, 2010 = 100": Labels the y-axis as “Index, 2010 = 100”.ylim = c(0, 250): Sets the limits for the y-axis to range from 0 to 250.

In summary, this code chunk generates Figure 5.9, a line plot that displays the trend of residential property prices across all regions over a specified period. Note that the regions are not labeled to avoid crowding the plot.

Figure 5.9: Basic Plot of Residential Property Prices - All Regions

To add labels in a less cluttered plot, you can manually select a subset of regions as shown in the following example:

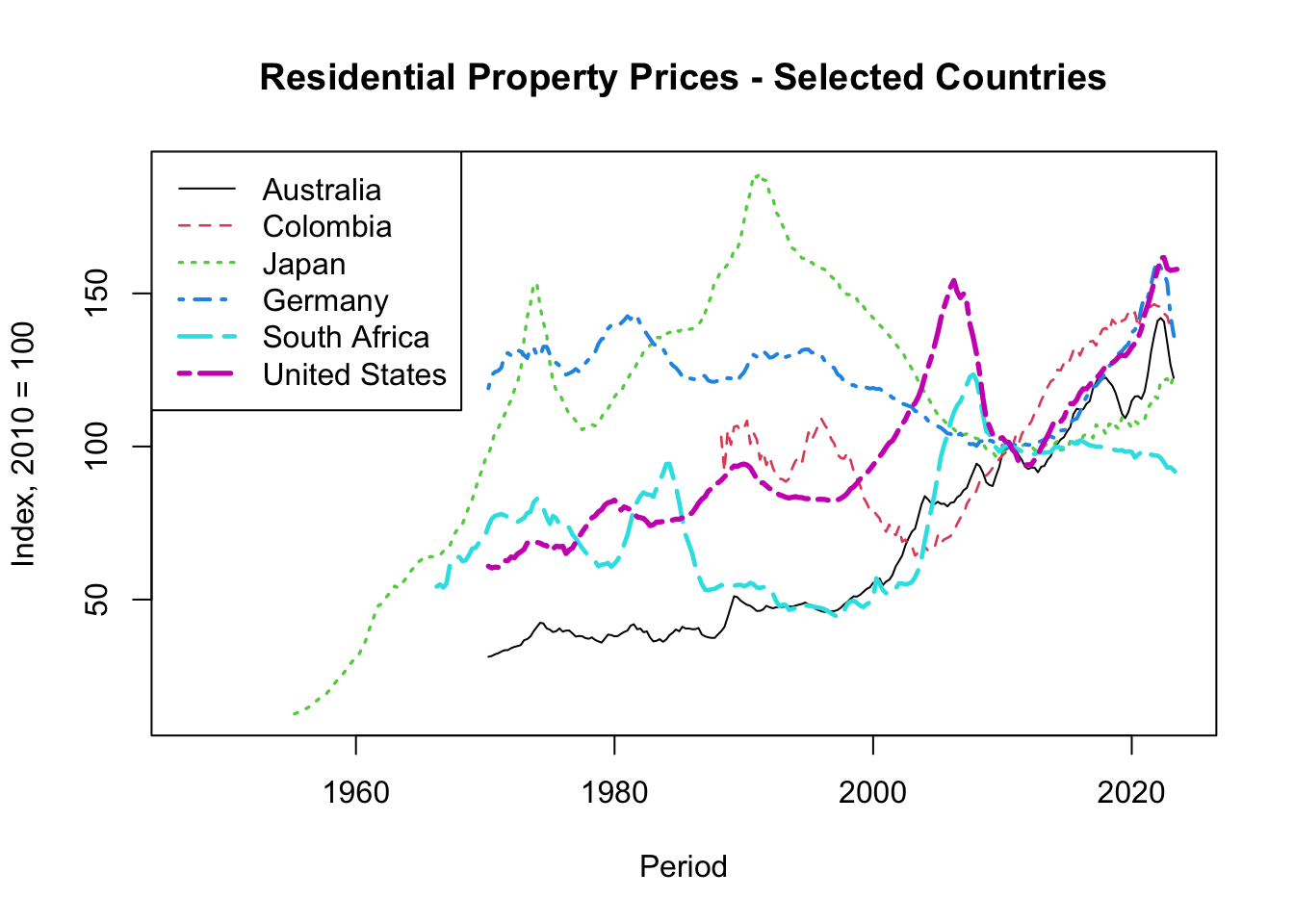

# Select variables to plot

selected_countries <- c(

"Australia", # Oceania

"Colombia", # South America

"Japan", # Asia

"Germany", # Europe

"South Africa", # Africa

"United States" # North America

)

# Multiple line plots

matplot(x = RPP_real_index_wide$Period,

y = RPP_real_index_wide[, selected_countries],

type = "l",

main = "Residential Property Prices - Selected Countries",

xlab = "Period",

ylab = "Index, 2010 = 100",

lty = 1:6, col = 1:6, lwd = 1 + 0:5 / 3)

legend(x = "topleft", legend = selected_countries,

lty = 1:6, col = 1:6, lwd = 1 + 0:5 / 3,

seg.len = 2, ncol = 1)This R code chunk creates a line plot for residential property prices for a selected group of countries. Here’s what each part of the code does:

selected_countries <- c(...): This line defines a vector namedselected_countriesthat contains the names of countries you want to plot. They are categorized by continent for clarity.matplot(x = RPP_real_index_wide$Period, y = RPP_real_index_wide[, selected_countries], type = "l"): Thematplot()function plots multiple lines. Thexargument specifies what should be on the x-axis (time period). Theyargument specifies which columns (countries) from the data frame should be plotted on the y-axis. Thetype = "l"specifies that lines should be used for plotting.main = "Residential Property Prices - Selected Countries": Sets the title of the graph.xlab = "Period", ylab = "Index, 2010 = 100": These arguments label the x-axis and y-axis, respectively.lty = 1:6, col = 1:6, lwd = 1 + 0:5 / 3: These arguments set the line types (lty), colors (col), and line widths (lwd) for the lines in the plot.legend(x = "topleft", legend = selected_countries, ...): Adds a legend at the top left of the plot. The legend shows which line corresponds to which country. The line types, colors, and widths are set similar to those in the plot.

Overall, this code chunk generates Figure 5.10, a line plot featuring residential property prices for the selected countries over time. The plot is customized with titles, labels, and a legend for better readability and interpretation.

Figure 5.10: Basic Plot of Residential Property Prices - Selected Countries

Layered Line Graph Using ggplot()